2023-11-13 08:32

Digital assets have seen strong gains in the last month due to excitement about the potential approval of bitcoin spot ETFs, but this bullish sentiment may be misplaced, the report said. Excitement about the potential approval of spot bitcoin exchange-traded-funds (ETF) has fueled a strong rally in digital assets over the past month, but the move higher seems overdone, JPMorgan (JPM) said in a research report last week. Bullish sentiment has been buoyed by two main arguments, the bank said. “A spot bitcoin ETF approval would help crypto markets to attract fresh/new capital as the newly-approved ETFs see inflows,” and the “approval would cement a win for the crypto industry and a setback for the Securities and Exchange Commission (SEC) thus making it more likely that going forward the SEC approach towards the crypto industry will soften,” analysts led by Nikolaos Panigirtzoglou wrote. The bank says it is skeptical of both arguments. Instead of new capital entering the crypto sector, it is more likely that existing capital will move from current bitcoin products such as the Grayscale Bitcoin Trust (GBTC), bitcoin futures ETFs and listed mining companies, into the newly approved spot ETFS. JPMorgan notes that such ETFs already exist in Canada and Europe and have gained “little interest from investors since their inception.” While the Ripple and Grayscale court rulings represent legal defeats for the SEC, “it is far from clear that the regulatory tightening of the crypto industry will lessen significantly going forward given how unregulated this industry is,” the report said. “U.S. crypto industry regulations are still pending and we do not believe U.S. lawmakers would shift their stance because of the above two legal cases especially with the memories from the FTX fraud still fresh,” the analysts wrote. The bitcoin halving, likely in April or May next year, is also cited as another bullish tailwind for crypto markets, the bank said, but this argument is “unconvincing” as the effect of the halving is unpredictable and is already priced in. CoinDesk’s parent company, Digital Currency Group, also owns Grayscale. https://www.coindesk.com/markets/2023/11/13/the-crypto-market-rally-looks-overdone-jpmorgan-says/

2023-11-10 22:09

There are overwhelming similarities between the FTX and MF Global bankruptcies — and one big difference. Halloween marked the 12-year anniversary of the collapse of MF Global, the eighth largest bankruptcy in U.S. history, where a major political donor caused a multi-billion dollar shortfall of customer segregated funds by transferring them to cover losses on proprietary trading. Sound familiar? James Koutoulas is co-founder of the Commodity Customer Coalition and trustee of the LetsGoBrandon.com Foundation. It should if you’ve been following the trial of FTX founder Sam Bankman-Fried, aka SBF, who was just convicted on seven counts of criminal charges and faces up to 110 years in prison. The federal criminal case was almost unprecedented in efficiency, resulting in a conviction less than a year after FTX collapsed and charges were brought. Although SBF’s trial was as speedy as they come, his hundreds of thousands of potential victims will likely have to wait a long time for restitution. An estimated $8 billion worth of customer assets were lost in the FTX fraud. While the exchange’s current leadership — led by bankruptcy expert John J. Ray III, of Enron fame — has been slowly clawing back some of those funds, it is still an open question how much and when any assets will be returned to FTX users. The quick criminal conviction of SBF stands in sharp contrast to a very similar case: MF Global. MF Global was a 200-year-old commodity broker which installed former Goldman Sachs co-CEO Jon Corzine as CEO in an attempt to turn the sleepy broker into an investment bank. Corzine then risked virtually all of MF Global’s firm capital into risky distressed European Sovereign Debt — at 30:1 leverage. Corzine used convoluted and offshore systems to hide this concentrated risk from credit rating agencies for 17 months waiting for his trade to hopefully come to fruition. But before that happened the risk was exposed, MF Global’s credit downgraded and the firm received a billion dollar margin call from its biggest lender, JPMorgan Chase. Corzine then ordered the falsification of a segregated account statement to give himself plausible deniability to transfer customer customer funds to meet his margin call. This transfer was done on taped lines and resulted in the first shortfall in customer segregated funds in U.S. history. Approximately $1.6 billion was lost. I was then a 30-year-old manager of hedge fund Typhon Capital Management and non-practicing attorney, but one who had never litigated nor taken a class in bankruptcy. Two of my customers had chosen to clear separately managed accounts with MF (then the world’s largest non-bank commodity broker), and so I did what I could to help by getting a temporary New York law license and filing an emergency motion on their behalf. From a void of action to the New York Times profiling my three person firm, putting us on the first page of the business section, the story went viral and over 1,000 people a day began calling our office asking for help. At Typhon, my little sister Diana handled so many calls she heard phones ringing in her sleep for weeks. One of those callers was John L. Roe, a commodity broker with 1,000 customer accounts at MF Global and a father in Congress, Phil Roe. John had the idea to start the Commodity Customer Coalition, a voluntary effort to coordinate resources, and wrote our white paper explaining the importance of the bankruptcy on the entire American economy. Before you know it, we were representing virtually all of the 38,000 customers pro bono with help from my Northwestern law professor, J. Samuel Tenenbaum, and Barnes and Thornburg lawyers Trace Schmelz and David Powlen, with Hillary Escadeja, Susan Osmanski and David Rosen rounding out our small but very capable team of volunteers. As mentioned, MF Global collapsed after running a $1.6 billion shortfall resulting in the freezing of $6.7 billion in customer assets and trader customers being kicked off the trading floor by security since their accounts were completely inaccessible. However, Corzine, a former U.S. senator and governor of New Jersey, was only questioned by the FBI a year after the bankruptcy. He was never even charged. In Obama’s last week in office, Corzine received a civil settlement with the U.S. Commodity Futures Trading Commission of only $5 million dollars despite the huge shortfall and his $300 million net worth. Like SBF who donated millions to political candidates, Corzine was one of President Obama’s largest donation bundlers and was also one of Hillary Clinton’s chief fundraisers. Notably, both Corzine and SBF were friends with Gary Gensler and had unprecedented access to him when Gensler chaired the CFTC and SEC, respectively. MF Global’s clients eventually received 101 cents on the dollar thanks in large part to the volunteer efforts of the Commodity Customer Coalition, which designed an efficient interim claims process, hammered the pair of bankruptcy trustees both in and out of court and before Congress and successfully pressured JPMorgan Chase into returning $1 billion in customer funds to the bankruptcy estate that Corzine improperly sent to the bank. It is my legal opinion that Corzine unquestionably committed fraud and violated federal laws in a regulated commodity broker that was publicly traded and also subject to regulations including Sarbanes-Oxley, which mandates a high level of internal controls (of which MF Global had virtually none). Further, Corzine took his customers’ money, and sent it to JPMorgan to meet margin calls in MF Global’s name which is exceedingly similar to SBF using FTX depositors’ funds to cover trading losses at his proprietary trading firm, Alameda Research. Corzine also likely committed perjury in congressional testimony. He said “I simply do not know where the money is” despite being on taped lines ordering the illicit transfers and abuse of customer liquidity to fund operations. When the Department of Justice, which had primary jurisdiction over his many alleged crimes, did not charge Corzine, the CCC drafted an indictment and charging memo for felony theft under Tennessee state law and presented it to the state attorney general, who did not bring charges, either. Time and again, we have been told that the crypto industry needs regulation in order to prosecute wrongdoers. When looking at the crypto industry and markets domiciled in the U.S., it is my sense that intellectually-honest advocates of good faith can disagree on whether a certain crypto token is a "security” or whether it must be traded on a registered exchange or broker, though since there are none, statutes and regulations need to be passed to provided for registered crypto exchanges. In fact, these issues, and many others, are vigorously winding their way through our federal courts system today (including in my suit- Koutoulas vs. SEC in SDFL, which moves to quash an administrative subpoena issued on the non-security letsgobrandon.com meme coin). The courts have already issued some important decisions; the federal appellate courts are being petitioned to weigh in, and like the graybeard case in SEC v. Howey (which essentially established securities regulations in the U.S. as known today), the U.S. Supreme Court will almost certainly be asked to make its mark. And that is only the judicial branch, Congress has also passed piecemeal legislation and is contemplating more comprehensive legislation. Crypto-haters howl that the industry is the Wild, Wild West claiming it has evaded U.S. financial regulation. MF Global is evidence “beyond a reasonable doubt” that the haters are delusional. Regulation is neither a cure-all nor preventative for crime. MF Global was a NYSE publicly-traded company registered with the SEC, CFTC, NFA, CME, FINRA and the Federal Reserve and none of those regulations prevented crime nor prosecuted it. In the end, MF’s shareholders and its customers, whose segregated accounts were supposedly sacrosanct pursuant to federal law and regulation, were all left holding an empty bag. The regulators and prosecutors? Crickets. While the lack of cryptocurrency statutes and regulation in the U.S. did push much of FTX’s fraud offshore, the U.S. still has sound anti-fraud laws that transcend regulatory regimes and are instead limited only by the will of prosecutors to bring cases against high-profile targets. But, between these two multi-billion dollar fraud cases, it was the major political donor operating in an unregulated industry who has been convicted while the other donor subject to six regulators was never even charged. Many cynics thought SBF’s millions in political donations would help him escape justice, but pending sentencing, that doesn’t seem to be true. So, does his conviction give us hope that the two-tier justice system in the U.S. isn’t as bad as we thought? Or was SBF’s criminality just too overwhelming to ignore? One thing’s for certain, the rise and fall of FTX proves that regulation is not a precursor for criminal prosecution, and rubs salt in the wounds of the 38,000 MF Global victims for whom justice was never served — despite that firm being regulated by virtually every financial regulator in the U.S. https://www.coindesk.com/consensus-magazine/2023/11/10/weve-seen-the-ftx-collapse-before/

2023-11-10 21:04

How exchange-traded funds and futures contracts can reach TradFi and turbocharge the growth of crypto markets. The price of bitcoin, the world's largest cryptocurrency by market cap, began climbing during the week of October 23 after spending much of the summer stuck around $26,000. It recently rose above $35,000 to touch its highest level since May 2022. This post is part of Consensus Magazine's Trading Week 2023, presented by CME. Why is bitcoin appreciating? Some point to signs that a slate of exchange-traded funds that hold actual bitcoin — known as spot bitcoin ETFs — may soon be approved by U.S. regulators. Such approval (if granted) will provide investors with additional products to access bitcoin exposure and may attract participants who may have been sitting on the side-lines . The approval of the futures-based ProShares Bitcoin Strategy ETF (BITO) made history in October 2021 as one of the strongest-ever ETF launches, amassing more than $1bn in assets in just two days, and continuing to attract interest. Another popular theory is tied to bitcoin's upcoming "halving." This pre-programmed adjustment to the blockchain cuts in half the reward miners receive for processing transactions and creating new bitcoin from the current 6.25 to 3.125 bitcoin per block. This event occurs after 210k blocks are mined or about every four years until the maximum supply (21MM) is reached. The next halving, Bitcoin’s fourth, is expected to happen by mid-April 2024. In the past, this event and the associated supply reduction has coincided with a strong run-up in bitcoin’s price and could potentially lead to pre- and post-halving volatility. The geopolitical and macro backdrop for the upcoming halving is very different from previous ones and the availability of regulated, robust and liquid Bitcoin futures and options from CME Group means firms have trusted and tested products to hedge their bitcoin price risk or gain exposure. Use futures to position your portfolio Investors who trade in the futures market usually have one of two aims: to either hedge the price of an asset by locking in a future price or to speculate on the price direction of an asset to seek to profit from the ups and downs of futures prices. CME Group Bitcoin and Micro Bitcoin and futures and options can help investors navigate cryptocurrency market risks and potentially profit from its opportunities. Micro Bitcoin futures traded volume has doubled from 5,9000 contracts in September 2023 to 11,9000 contracts traded in October 2023 while Bitcoin futures witnessed a 38% increase in daily volume to 13,300 contracts over the same period. Why Trade CME Group Cryptocurrency Futures? Cryptocurrency futures bring three main advantages for investors. 1. The contract is cash-settled in USD. There is no need to custody the coin, which removes the risk of having to safely store it. That means you don’t need to have a wallet, worry about hackings, or insurance. The futures simply track the price of bitcoin or ether, and settle in USD, so, by trading cryptocurrency futures instead of the coins themselves, investors can bypass several operational hurdles. 2. They are CFTC-regulated contracts. That means they offer several customer protections. For example, your funds are fully segregated and each trade is centrally cleared. CME Group’s clearing house becomes the buyer to every seller and the seller to every buyer. This substantially mitigates counterparty risk from the trade. 3. Futures make it easier for investors to short. No "locate" or borrow is necessary, just simply sell to gain short exposure. Bitcoin and ether are no strangers to volatility. While some investors might embrace that, others are far more risk-averse. Selling futures contracts could well play a part in their strategy. Investors who like more risk can sell (short) futures to try and profit from bitcoin or ether’s downside moves. Other investors, meanwhile, can sell (short) futures to hedge the bitcoin or ether they already own. This way, they can offset some losses if their crypto portfolio takes a dive. Moreover futures offer investors more precision to fine tune exposure and allow them to control a large contract value with a smaller amount of capital. One Micro Bitcoin futures contract (ticker: MBT) is set to one-tenth of a bitcoin, which is 50 times smaller than a full-sized contract (ticker: BTC). One Micro Ether futures contract (ticker: MET) is one-tenth of an ether, which is 500 times smaller than its full-sized counterpart (ticker: ETH). The notional size for MBT is about $3,500 while for MET, it is about $200 (at current market prices). If you are buying bitcoin or ether on a spot exchange, you will need to fully fund the position before you trade. An advantage with futures is that you only need to put down the initial margin requirement, or the amount of money you need as collateral to open your trade. Institutional interest in Bitcoin futures has steadily climbed. Open interest, a measure of client demand, hit an all-time high of 20,380 contracts on October 25, equivalent to 101,900 bitcoin, representing $3.5 billion in notional value. Similarly, the number of large open interest holders (LOIH) of CME Group’s Bitcoin futures grew to a record 122 on October 24 (LOIH for Cryptocurrency futures is defined by the CFTC as an entity that holds at least 25 contracts). This is further proof that institutional investors are warming up to bitcoin and positioning their portfolios amid renewed optimism. Retail investors, too, seem to have played their part, as evidenced by the uptick in futures-based ETF’s AUM. The rolling five-day volume in ProShares’ industry-leading Bitcoin Strategy ETF (BITO) jumped by a staggering 420% to $340 million last week. BITO invests in CME Group Bitcoin futures. CME Group futures are not suitable for all investors and involve the risk of loss. Full disclaimer. Copyright © 2023 CME Group Inc. https://www.coindesk.com/consensus-magazine/2023/11/10/getting-ready-for-bitcoins-catalysts/

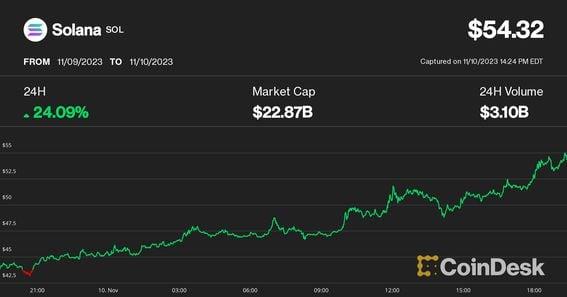

2023-11-10 19:13

The Solana token's massive rally this year increases the odds that FTX customers will recoup all their lost money. Solana's native token SOL has rallied 20% in the last 24 hours, continuing a three-week upswing that erased the asset's yearly losses – and then some. The token was trading hands near $54 at press time according to CoinDesk market data. It had last held that level in the weeks following Terra Luna's market-shattering collapse in May 2022. The price surge comes on the heels of Solana's annual conference and in spite of market jitters over going-on at FTX Group, a major holder of the SOL token. That bankrupt company has sent mixed messages about what it plans to do with its sizable stake. SOL's price jump could prove to be a win for the many creditors of FTX. The asset is now trading in a range that will make customers of the crypto exchange whole, according to Thomas Braziel, the CEO of 117 Partners, a company that closely follows the distressed asset markets. Sam Bankman-Fried was just convicted for stealing that customer money. Of course, that would require SOL to at the very least hold this level for possibly years. Much of FTX's SOL holdings are locked up until 2027 or later. https://www.coindesk.com/markets/2023/11/10/solanas-sol-rallies-20-in-a-day-erasing-woes-of-past-18-months/

2023-11-10 18:37

Stronger interest from institutional investors and a market with relatively few sellers could mean we’ve entered a new phase of the market, say FalconX’s Vivek Chauhan and David Lawant. It was hard not to take notice of the “uptober” crypto rally. Bellwether BTC was up over 35% since October, and assets such as LINK and SOL are up two or three times that much. Less explored, though, are the liquidity trends underpinning this price action. Observing these can help us gauge where we are in the cycle and thus navigate what the future market might hold. This post is part of Consensus Magazine's Trading Week, presented by CME. As we highlighted for CoinDesk earlier in the year, price changes with low trading volumes are less reliable indicators than those with higher volumes. Low volumes suggest limited market participation at a particular price level, potentially leading to greater price volatility and reduced market depth. Conversely, higher trading volumes signify broader market participation, indicating a stronger consensus and offering a more dependable basis for price movements, thereby bolstering the credibility of the signal. Trade volume recovery in BTC and ETH, the most watched liquidity metric, is eye-catching. Two of the top-15 trading volume days since the market top two years ago were recorded during this recent rally. And most of the other high-volume days happened as dramatic company failures were taking place in 2022, or as several mid-sized U.S. banks got into difficulty in March 2023. BTC Spot volumes, which until September were breaking three-year lows, have steeply recovered and are now approaching six-month highs. But this is not the whole story. Digging deeper into liquidity trends can provide us further insight. Strong action in derivatives, especially CME Futures open interest (OI) in BTC and ETH just crossed the $20 billion mark for the first time since the FTX meltdown in November 2022, led by BTC on the back of excitement around the highly anticipated U.S. spot ETF launch. Notably, but perhaps not surprisingly, this increase is led by institutional capital. The CME, a favorite venue for large traditional finance companies to get crypto exposure, gained the most market share across all venues and is close to overtaking Binance as the leading BTC futures exchange by OI. A similar trend can also be seen on options. Open interest in BTC options just crossed $16 billion, and volumes are now at all-time highs. Much of this action is translated to spot prices because a relevant part of these flows is likely hedged into spot. There’s a flipside: a more pronounced derivatives market means there’s more inherent leverage in the system. So the risk of forced liquidations exacerbating price movements will likely increase from here. Spot Order books tightened and revealed a relative lack of sellers Order book depth – an alternative liquidity metric that gauges how much capital would be required to change the asset price by a certain percentage given the limit orders in place at any time – has tightened over the past few months, despite the strong price increases. The chart below shows the 1% depth of book for BTC and ETH (top and bottom, respectively) in U.S. dollars and native units (left and right, respectively) over 2023. There is a decrease over the past 3-5 months, whichever chart you look at. And the sell side of the orderbook is trending toward shrinking by more than the buy side, suggesting a lack of sellers relative to buyers. Busy derivatives dynamics meet a tight spot market The chart below shows annualized realized volatility for BTC and ETH using a seven-day lookback period to capture the recent price surge. Although volatility picked up recently, it remains relatively low for both BTC and ETH, as it did not break above 63% on an annualized basis, which is below the median value during the previous bull market in 2020 and 2021. This matters to liquidity because volatility usually drives higher trading activity. BTC’s current spot volumes adjusted by volatility are already in the top quartile of the 2020/2021 bull market cycle. This rally feels different Stronger interest from more traditional institutional investors and a market with relatively few sellers amid increasing but still relatively low volatility point to the market shifting gears to a new phase. Looking forward, even if the possibility of interim corrections grows from there and the macro environment remains cloudy, this rally might be the start of the next bull market. CoinDesk does not share the editorial content or opinions contained within the package before publication and the sponsor does not sign off on or inherently endorse any individual opinions. https://www.coindesk.com/consensus-magazine/2023/11/10/liquidity-trends-suggest-uptober-could-be-the-start-of-a-new-crypto-bull-run/

2023-11-10 18:29

The proposed stablecoin, which tokenizes ownership of Treasuries, mentions BlackRock, Circle, Fireblocks and Coinfirm as "institutional partners." A new addition to the current convergence trend between crypto and traditional finance is Midas, a stablecoin backed by U.S. Treasuries that's planning to unleash its stUSD token on decentralized finance (DeFi) platforms like MakerDAO, Uniswap and Aave in the coming weeks, according to a presentation deck seen by CoinDesk. The Midas stablecoin project intends to buy Treasuries via asset manager BlackRock and use Circle Internet Financial's USDC stablecoin as an on-ramp, according to the deck. Custody technology provider Fireblocks and blockchain analytics firm Coinfirm are also listed as institutional partners. Yields offered by assets in traditional finance (TradFi) like U.S. Treasuries currently exceed yields on conventional DeFi products. The solution, as the Midas presentation deck states, is to tokenize TradFi products so they're available in the DeFi ecosystem. So-called tokenized real-world assets are a hot corner of the digital-asset space, drawing attention from TradFi firms that have long tried to get key parts of markets and finance onto blockchain infrastructure given the potential efficiencies. Treasuries have been an area of focus, with large growth in 2023. The new Midas stablecoin, which aims to onboard with DeFi platforms during this quarter ahead of a retail launch early next year, joins an interesting trend in yield bearing stablecoins, such as Mountain Protocol and Ondo Finance. (The proposed Midas stUSD project is not to be confused with the now-defunct DeFi investment firm Midas.) The Midas team includes Fabrice Grinda, founder and executive chairman of blank check company Global Technology Acquisition Corp. (GTAC); and Dennis Dinkelmeyer, who is vice president of GTAC. The Midas stUSD token is 100% backed by U.S. Treasuries and issued as a debt security under German law, according to the deck. "Funds are held with a regulated custodian in segregated accounts (BlackRock)," Midas said in the presentation deck. "Midas is fully compliant with European Securities Regulation and Anti-Money Laundering law. Transfer of token represents transfer of legal rights to the underlying." Grinda and Dinkelmeyer did not respond to requests for comment by press time. https://www.coindesk.com/business/2023/11/10/meet-midas-a-new-yield-bearing-stablecoin-investing-in-us-treasuries/