2025-06-03 06:17

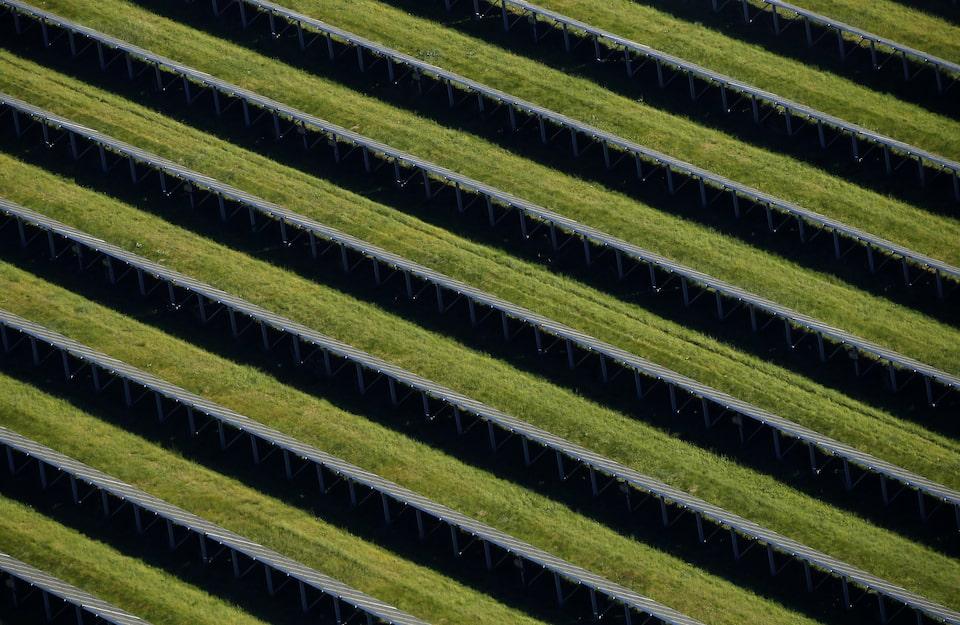

LITTLETON, Colorado, June 3 (Reuters) - Eastern Europe is often overlooked in discussions about solar power generation in Europe, where the likes of Germany and Spain dominate the growth in deployed solar electricity production. But solar capacity across the nine largest solar producers in Eastern Europe has grown at over twice the pace of Europe as a whole over the past five years, and has helped Eastern Europe double its share of regional solar production since 2019. Sign up here. At least six Eastern European nations will generate over 20% of their total monthly utility-supplied electricity from solar farms this summer, when regional solar radiation levels hit their annual peak. In many of these countries, the rapid solar growth is displacing or curtailing output from coal and natural gas power plants, and is leading to a steeper fall in power sector emissions in Eastern Europe than across the overall continent. Continued growth in solar capacity is expected across Eastern Europe over the medium term as nations there try to curb reliance on imported fossil fuels. This in turn should further elevate the area's importance in driving Europe's broader energy transition momentum. REGIONAL LEADERS Nine nations across Eastern Europe are driving the region's solar expansion, according to data from energy think tank Ember. In descending order of embedded utility-scale solar capacity at the end of 2024, those nations are: Poland (20.2 gigawatts of capacity); Hungary (7.7 GW); Romania (4.7 GW); Czech Republic (4.2 GW); Bulgaria (4 GW); Lithuania (2.6 GW); Estonia (1.3 GW); Slovakia (1 GW) and Latvia (0.5 GW). Combined solar capacity of those countries was roughly 46 GW at the end of 2024, or roughly 13% of Europe's total 361 GW of solar capacity, data from think tank Ember shows. That collective solar capacity footprint compares to just 9 GW in the same countries in 2019, and so represents a more than 450% jump in utility solar capacity in those countries in just the past five years. Over the same period, solar capacity across Europe as a whole increased by a more modest 145%, and included an 89% rise in German solar capacity and a 246% climb in solar capacity in Spain. OUTPUT IMPACT The volume of utility-scale electricity production from solar farms has surged across Eastern Europe in response to the higher capacity footprint. In 2019, total solar electricity output across the nine top solar producers in Eastern Europe was around 9 terawatt hours, but was nearly 42 TWh in 2024. That nearly fivefold rise in Eastern European solar output contrasted with just over a doubling in solar output for Europe as a whole over the same period, from around 153 TWh to 361 TWh in 2024. The share of solar power within Eastern Europe's combined electricity generation mix has also sharply climbed since 2019, and exceeds the solar share of electricity production within Europe overall. Solar accounted for just 2% of Eastern Europe's electricity supplies in 2019, but topped 10% for the first time in 2024. For Europe as a whole, solar accounted for a 7% share in 2024, up from a 3% share in 2019. GROWTH MARKETS Several Eastern European nations generated over 20% of total monthly electricity supplies from solar farms during the peak summer months of 2024, and are primed to generate even larger solar shares this summer following further capacity growth. Lithuania, Hungary and Estonia all generated more than a third of their total monthly utility-supplied electricity from solar farms during June through August in 2024, Ember data shows. Bulgaria, Latvia and Poland generated 20% or more of their electricity from solar farms. This summer, following the build-out of further capacity across all of Europe, solar's share of the generation mix looks set to swell further - especially in Poland where installed capacity has grown by more than 25% since early 2024. This expanded solar footprint will not only help push Poland's total solar electricity output to a new record this year, but will also serve to further reduce the country's overall power emissions. Coal remains Poland's primary power source, but a near doubling in clean electricity output since 2019 - largely due to a nearly 2,000% rise in solar generation - has helped the country's utilities cut coal power output by 26% in that period. Lower coal-fired generation has in turn cut Poland's power sector emissions from fossil fuel use by 23% or by 22 million metric tons of CO2 since 2019. As Poland is Eastern Europe's largest polluter, the drop in the country's discharge has helped lower regional pollution, too, by 26% since 2019 to 163 million tons of CO2 in 2024. This year, thanks to further increases in solar generation and additional cuts to coal power production, overall emissions across Eastern Europe could fall further and play a key role in advancing Europe-wide energy transition efforts. The opinions expressed here are those of the author, a columnist for Reuters. https://www.reuters.com/markets/commodities/eastern-europes-stealthy-surge-solar-generation-maguire-2025-06-03/

2025-06-03 06:06

Global refining margins hit a 14-month high in May Capacity closures in Europe, US, have tightened fuel supply Margins also boosted by summer peak fuel demand, relatively low stocks LONDON, June 3 (Reuters) - Refiners across the globe are reaping unexpected profits from producing key fuels in recent weeks, offering an ailing sector respite before an anticipated weakening later this year, as plant closures have tightened fuel supply needed to meet peak summer demand. The strength in fuel markets contrasts with crude oil prices falling to a four-year low in May, after OPEC+ unwound output cuts faster than planned. It also suggests demand has so far proved resilient despite ongoing concerns about the impact of tariffs. Sign up here. "Margins are strong because the balance of products - supply and demand - is still tight," said Sparta Commodities analyst Neil Crosby. Refining margins reflect the profits a plant makes from processing crude oil into fuels such as gasoline or diesel. Just a few months ago, oil majors were warning 2025 would be a bleak year for refining. TotalEnergies and BP reported lower first-quarter profits because of weaker earnings from fuels. Refiners have broadly struggled with waning demand from economic slowdowns, an increasing uptake of electric vehicles, and competition from newer plants in Asia and Africa. Global composite refining margins reached $8.37 per barrel in May 2025, according to consultancy Wood Mackenzie, their highest since March 2024, but still much lower than the $33.50 average in June 2022 during the post-pandemic demand recovery and in the wake of Russia's invasion of Ukraine. Closures in the United States and Europe have slowed global net refinery capacity growth below demand growth, helping to make operational refineries relatively more profitable. Global diesel supply could decline by 100,000 barrels per day (bpd) year-on-year in 2025, while demand will drop 40,000 bpd, according to energy consultancy FGE. Gasoline supply will decline by 180,000 bpd, with demand rising by 28,000 bpd. "We are therefore seeing a tighter product market for key transport fuels which is exerting upwards pressure on margins, much to the relief and joy of regional refiners," said FGE's head of refined products Eugene Lindell. Refiners of all fuel-producing configurations are benefitting from current margins, FGE's head of refining Qilin Tam added, as light fuels such as gasoline and heavy products like fuel oil have recently increased. In Europe, closures include Petroineos' Grangemouth refinery in Scotland and Shell's Wesseling facility this year, as well as a part closure of BP's Gelsenkirchen refinery. In the U.S., LyondellBasell's Houston refinery was shuttered this year, while Phillips 66's Los Angeles refinery and Valero's Benicia refinery are set to close in October 2025 in April 2026 respectively. Unplanned refinery shutdowns have also compounded the impact of closures. A power outage across the Iberian peninsula on April 28 took around 1.5 million bpd of refinery capacity offline, JPMorgan noted, with 400,000 bpd of that still shut in two weeks later. Two of the world's major new refinery projects, Nigeria's giant Dangote refinery, and Mexico's Olmeca refinery, both had unplanned outages on gasoline-producing units in April. TIGHTER BALANCES Fuel inventories at key hubs have declined this year, creating extra demand for refinery production heading into the peak summer season. Stocks in the OECD region, which includes the U.S., EU and Singapore, fell by 50 million barrels over January-May, according to JPMorgan analysts. "This significant reduction in product stocks has underscored the resilience in product prices," the analysts said. Global fuel demand in the northern hemisphere is highest in summer as motoring and air travel increase. In the Middle East, heavy fuel oil demand peaks in summer to meet cooling demand when temperatures soar. "Strength in the northern hemisphere summer demand growth is where we see some support to margins," said Rystad Energy analyst Janiv Shah. U.S. refining executives have been upbeat on demand, while noting relatively low stocks. "Our current gasoline supply outlook is for those inventories to continue to tighten," Phillips 66 executive vice president Brian Mandell said on the firm's first-quarter earnings call. Marathon Petroleum's domestic and export businesses were seeing steady demand for gasoline, and growth for diesel and jet compared to 2024, CEO Maryann Mannen said on its earnings call. However, analysts have warned that the current strength may soon fade as demand is hit by trade wars, and as fuel production rises as plants look to profit from higher margins. "We have the view that there is a bit of a short-term bump," Wood Mackenzie analyst Austin Lin said. Global oil demand growth is set to average 650,000 bpd for the remainder of 2025, falling from just short of 1 million bpd in the first quarter as trade uncertainty weighs on the global economy, according to the International Energy Agency. "Refiners should be hedging everything now, as I think this is as good as it gets for them," a veteran oil trader, who asked not to be named, added. https://www.reuters.com/business/energy/global-oil-refiners-see-short-term-boost-higher-margins-2025-06-03/

2025-06-03 06:06

BP's net debt reached $27 billion by end of Q1 CEO aims to reduce net debt to $14-$18 billion by 2027 Shares have underperformed rivals since strategy reset in February LONDON, June 3 - BP has jumped from crisis to crisis in recent years, severely eroding the British firm’s stature as one of the world's leading oil companies. Given the increasingly challenging dynamics in today’s oil market, BP may finally need to accept that it is no longer a true oil major and can’t keep managing cash like one. The exclusive Big Oil club of Exxon Mobil (XOM.N) , opens new tab, Chevron (CVX.N) , opens new tab, Shell (SHEL.L) , opens new tab, TotalEnergies (TTEF.PA) , opens new tab and BP (BP.L) , opens new tab has for decades been synonymous with sprawling upstream and downstream oil and gas operations, solid balance sheets and long-term strategies that have helped generate sizeable, stable shareholder returns. Sign up here. But BP hasn't ticked most of these boxes for years, having dealt with a succession of crises over the past 15 years that have slashed its market cap and left it financially vulnerable and lacking clear strategic direction. Most recently, a failed foray into renewables and a management scandal saddled the company with a ballooning debt pile as it struggles to revert back to oil and gas. CEO Murray Auchincloss acknowledged the need for change when he unveiled in February a fundamental strategy reset that includes reducing spending to below $15 billion to 2027, cutting up to $5 billion in costs and selling $20 billion of assets in an effort to boost performance and rein in ballooning debt. The plan also reset the rate of shareholder returns to 30-40% of operating cash flow. But the reset has done little to alleviate investor concerns. BP's shares have declined by 18% since the strategy update, underperforming rivals. Piling on the pressure, activist shareholder Elliott Management, which has recently built a 5% position in the company, has indicated it wants BP to cut spending even more. There is, therefore, clearly a need for deeper change. CHANGE OF GUARD While it may be challenging for the 116-year-old company to admit that it can no longer carry the same financial heft it once did, accepting reality will offer the company’s leadership an opportunity to reduce some of its commitments to investors, particularly its share repurchase programme. All energy majors today have multi-billion-dollar buyback programmes that send capital back to shareholders, helping to attract investors who may be wary about the future of fossil fuel demand. But BP's buybacks feel like a luxury that is out of synch with its financial woes. In its first quarter results released in February, BP said it would buy back $750 million over the following three months. That was lower than the $1.75 billion in the previous three months, but even at this reduced rate, this would still total $3 billion per year. That doesn’t seem prudent, especially given the 20% drop in oil prices to around $65 a barrel this year and the darkening economic outlook. Auchincloss' financial objectives assume a Brent oil price of $70, meaning the Canadian CEO will most likely struggle to meet his targets without borrowing further. DEFINE DEBT Removing the annual $3 billion buyback would certainly upset investors, but it would go a long way towards reducing BP’s net debt to between $14 and $18 billion by 2027, compared with $27 billion at the end of March 2025. The “ground zero” of BP's financial decline was the deadly 2010 Deepwater Horizon disaster in the Gulf of Mexico, which generated $69 billion in clean-up and legal costs , opens new tab. The company continues to pay out over $1 billion per year in settlements. The financial shock forced BP to sell billions of dollars of assets and issue huge amounts of debt to foot the bill. Its market value dropped to around $77 billion today compared to $180 billion in 2010. BP's debt-to-capitalization ratio, known as gearing, reached 25.7% at the end of the first quarter of 2025, significantly higher than those of other oil majors, including Shell’s 19% or Chevron’s 14%. And, importantly, BP's current $27 billion net debt figure omits several major liabilities held on its books. This includes $17 billion in hybrid bonds, an instrument that has qualities of both equity and debt, including a coupon that must be paid or accrued. While companies may issue hybrids for many reasons, including maintaining flexibility, they often do so in part because rating agencies do not treat hybrids as regular debt, which flatters the issuer's leverage ratios. Anish Kapadia, director of energy at Palissy Advisors, calculated BP's adjusted net debt hit $86 billion at the end of the first quarter of 2025, when including net debt, hybrids, Gulf of Mexico liabilities, leases and other provisions. Ultimately, cutting the buybacks should enable BP to tame its huge debt pile and repair its balance sheet faster. That, in turn, should create a strong foundation for rebuilding investor confidence. The departure of current BP Chairman Helge Lund in the coming months could be a good opportunity for the company to consider such radical change. It’s unclear who will take this job, but one qualification for whoever succeeds Lund should be a much-needed sense of financial realism. Want to receive my column in your inbox every Thursday, along with additional energy insights and trending stories? Sign up for my Power Up newsletter here. https://www.reuters.com/markets/europe/bp-needs-scrap-its-big-oil-mentality-its-buybacks-bousso-2025-06-03/

2025-06-03 05:42

OECD warns of global economic slowdown due to trade war Trump and Xi to meet this week - White House US job openings rise, factory orders drop unexpectedly Euro Zone inflation eases to ECB target Crude prices rise amid Ukraine war and Iran nuclear deal tensions NEW YORK, June 3 (Reuters) - U.S. stocks advanced and the dollar rebounded on Tuesday as investors weighed progress in ongoing U.S. tariff talks and lowered economic expectations ahead of Friday's crucial U.S. employment report. All three major U.S. stock indexes ended the session with gains, with chips (.SOX) , opens new tab putting the tech-heavy Nasdaq out front following White House assurances that U.S. President Donald Trump will likely meet Chinese President Xi Jinping this week to address trade disputes between the world's two largest economies. Sign up here. Gold backed down from a nearly four-week high as the greenback strengthened. "It's hard to know what's really driving things today," said Chuck Carlson, CEO of Horizon Investment Services in Hammond, Indiana. "There seems to be a little bit more comfort that the economy is not going into recession, and there might be a bit of front-running here in the sense we have a jobs report that's going to be coming out and investors want to get on the right side of that before it's released." While the Trump administration pressed U.S. trading partners to provide their best offers by Wednesday, the protracted negotiations and moving deadlines have prompted economists to dial back economic expectations due to fallout from Trump's trade war. The Organization for Economic Cooperation and Development (OECD) said the global economy is on course for a more drastic slowdown than it had expected only a few months ago. It cited Trump's trade war, and warned of even weaker growth as protectionism increases, fueling inflation and disrupting supply chains. The United Nations' International Labor Organization (ILO) downgraded its global employment forecast, citing worsened economic conditions from trade tensions. "Maybe that's helping U.S. markets," Carlson added, noting that the weaker global economic growth projections could be encouraging investors to move money back into U.S. The U.S. Labor Department reported that the number of unfilled U.S. jobs unexpectedly rose in April, while new orders for factory-made goods posted a steeper drop than analysts had anticipated. Investors are now focused on the May employment report due on Friday. Economists polled by Reuters expect the U.S. economy added 130,000 jobs last month, with the unemployment rate standing pat at 4.2%. The Dow Jones Industrial Average (.DJI) , opens new tab rose 214.16 points, or 0.51%, to 42,519.64, the S&P 500 (.SPX) , opens new tab rose 34.43 points, or 0.58%, to 5,970.37 and the Nasdaq Composite (.IXIC) , opens new tab rose 156.34 points, or 0.81%, to 19,398.96. European stocks ended nominally higher as investors weighed trade anxieties against a report that euro zone inflation has eased below the European Central Bank's target, paving the way for further policy easing. MSCI's gauge of stocks across the globe (.MIWD00000PUS) , opens new tab rose 2.64 points, or 0.30%, to 885.52. The pan-European STOXX 600 (.STOXX) , opens new tab index rose 0.09%, while Europe's broad FTSEurofirst 300 index (.FTEU3) , opens new tab rose 3.80 points, or 0.17% Emerging market stocks (.MSCIEF) , opens new tab rose 3.67 points, or 0.32%, to 1,157.44. MSCI's broadest index of Asia-Pacific shares outside Japan (.MIAPJ0000PUS) , opens new tab closed higher by 0.37%, to 609.73, while Japan's Nikkei (.N225) , opens new tab fell 23.86 points, or 0.06%, to 37,446.81. The dollar bounced back from a six-week low, even as concerns persisted over potential economic damage in the wake of Trump's trade war. The dollar index , which measures the greenback against a basket of currencies including the yen and the euro, rose 0.71% to 99.28, with the euro down 0.62% at $1.137. Against the Japanese yen , the dollar strengthened 0.93% to 144.02. Longer-dated U.S. Treasury yields dipped as investors awaited new developments in trade talks, but were off initial lows in the wake of economic data. The yield on benchmark U.S. 10-year notes fell 1 basis point to 4.452%, from 4.462% late on Monday. The 30-year bond yield fell 1.8 basis points to 4.9769% from 4.995% late on Monday. The 2-year note yield, which typically moves in step with interest rate expectations for the Federal Reserve, rose 0.8 basis points to 3.953%, from 3.945% late on Monday. Crude prices extended gains, supported by geopolitical concerns as the war in Ukraine intensified and Iran appeared poised to reject a U.S. nuclear deal proposal. U.S. crude rose 1.42% to settle at $63.41 per barrel, while Brent settled at $65.63 per barrel, up 1.55% on the day. Gold prices retreated from a nearly four-week high amid profit-taking and in opposition to the strengthening dollar. Spot gold fell 0.78% to $3,352.87 an ounce. U.S. gold futures fell 0.59% to $3,350.60 an ounce. https://www.reuters.com/world/china/global-markets-wrapup-1-2025-06-03/

2025-06-03 05:27

MUMBAI, June 3 (Reuters) - The Indian rupee held steady on Tuesday after a slight dip at open, while implied volatility eased further as traders awaited key domestic and U.S. events this week. The currency slipped past 85.50 at open, down about 15 paisa from Monday, hitting a low of 85.56. The currency has been rangebound post that and was last quoting at 85.47 to the U.S. dollar. Sign up here. "The rupee has been trading in a relatively narrow range last few days, and today appears no different," said a currency trader at a private bank. "It's essentially a wait-and-watch scenario now, with markets looking for either flows or headlines to provide a directional cue." The dollar was broadly under pressure, weighed down by concerns over the U.S. fiscal deficit and lingering uncertainty around trade policy. However, the rupee failed to capitalise on the modest uptick on most Asian currencies. The rupee's implied volatility has been sliding lower, thanks to the rangebound spot. The 1-month implied volatility is now at 5%, having peaked at over 7% in the second week of May. Traders highlighted two key events on their radar this week - the Reserve Bank of India’s policy decision on Friday and the U.S. non-farm payrolls report scheduled for the same day. The RBI is widely expected to cut rates for the third straight meeting on Friday given the benign inflation backdrop. Later that day, the U.S. non-farm payrolls report for May could influence expectations around potential Federal Reserve rate cuts, depending on the strength of labour market data. https://www.reuters.com/world/india/rupee-steady-after-initial-dip-implied-volatility-softens-2025-06-03/

2025-06-03 05:12

TSMC CEO sees US tariffs having some impact, AI demand strong TSMC has discussed tariffs with US government, CEO says Company has no plans to build factories in Middle East TSMC margins impacted by Taiwan dollar's appreciation HSINCHU, Taiwan, June 3 (Reuters) - Taiwan's TSMC (2330.TW) , opens new tab said on Tuesday that U.S. tariffs were having some impact on the company and had been discussed with Washington, but demand for artificial intelligence (AI) remains strong and continues to outpace supply. U.S. President Donald Trump's trade policies have created much uncertainty for the global chip industry and TSMC, the top producer of the world's most advanced semiconductors whose customers include Apple (AAPL.O) , opens new tab and Nvidia (NVDA.O) , opens new tab. Sign up here. Chief Executive C.C. Wei, speaking at TSMC's annual shareholders meeting in the northern Taiwanese city of Hsinchu, said the company had not seen any changes in customer behaviour due to tariff uncertainty and the situation might become clearer in coming months. "Tariffs do have some impact on TSMC, but not directly. That's because tariffs are imposed on importers, not exporters. TSMC is an exporter. However, tariffs can lead to slightly higher prices, and when prices go up, demand may go down," he said. "If demand drops, TSMC's business could be affected. But I can assure you that AI demand has always been very strong and it's consistently outpacing supply." In April, the company, the world's largest contract chipmaker, gave a bullish outlook for the year on robust demand for AI applications. Wei said TSMC had been talking to the U.S. Department of Commerce about tariffs, expressing concern early on that the levies could increase production costs in the country where it is investing $165 billion to build new factories, as some equipment purchased from U.S. suppliers is made in Asia. "The U.S. commerce department said this is open for discussion, but how long that will take remains unclear," he added. "The real point is that we are in active communication, because only through understanding can they realise the consequences." Wei said he had told Trump the extra $100 billion investment, which he announced standing next to the president in March, would be difficult to complete within five years. "He said, 'Mr Wei, do your best, that's good enough.'" Asked about media reports that the company had been looking at building chip factories in the United Arab Emirates, Wei said TSMC had no plans for any such plants in the Middle East because it was "not very likely" they would have customers there. Domestically, TSMC's margins are being pressured by the recent appreciation of the Taiwan dollar , which Wei said had reduced its gross margin by more than 3 percentage points. TSMC also faces broader political risk as China steps up military pressure on democratically and separately governed Taiwan, which Beijing views as "sacred" Chinese territory. "If something happens that we don't want to happen, it's a matter for governments, not for TSMC alone," Wei said, responding to a question about a possible crisis in the Taiwan Strait. https://www.reuters.com/sustainability/climate-energy/tsmc-says-tariffs-have-some-impact-ai-demand-robust-2025-06-03/