like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: EUR-USD hits 4-month high

Key takeaways

- The EUR has outperformed many other currencies so far in March…

- …supported by the prospect of Germany’s fiscal boost and higher European bond yields.

- The ECB cut rates again in March, but the path for future easing is still in doubt; the risk of US tariffs looms ever larger.

Following Germany’s moves towards looser fiscal policy, the EUR has become the second best performing G10 currency so far this month (Chart 1) and EUR-USD climbed to a 4-month high (Bloomberg, 6 March 2025). On 4 March, Germany's incoming coalition partners, CDU/CSU and SPD, announced a massive fiscal programme of infrastructure and defence spending, involving constitutional changes. The government aims to table the package in parliament before 25 March. The changes will require two-thirds majority in the lower and the upper house, which seems likely, in our economists’ view. The EU has potentially created EUR650bn of fiscal space for defence by the activation of the escape clause from fiscal rules and could provide EUR150bn of loans for defence investment.

Allocating funds is one thing, but governments may find it difficult to spend it within the expected timeframe. It is worth remembering that Germany’s 2022 EUR100bn defence fund has almost all been allocated, but less than 25% had been spent by January 2025. Looser fiscal policy will support growth but by how much and over what period remains uncertain. Meanwhile, the risk of US tariffs looms ever larger. A White House announcement imposing trade tariffs on the EU is expected by 2 April.

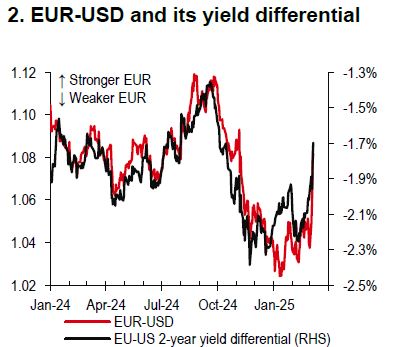

While the FX market is being dominated by big picture topics, like US trade policy and German fiscal policy, EUR-USD has been basically following what its 2-year yield differential has implied (Chart 2). This means the key to the EUR remains the policy outlook for the European Central Bank (ECB).

Source: Bloomberg, HSBC

Source: Bloomberg, HSBC

On 6 March, the ECB cut its rate by 25bp, taking the key deposit rate and the main refinancing rate down to 2.50% and 2.65%, respectively. The decision came as expected, bringing the total easing since June 2024 to 150bp. The ECB said, “monetary policy is becoming meaningfully less restrictive”, and “especially in current conditions of rising uncertainty, it will follow a data-dependent and meetingby-meeting approach". Over the past few days, markets have focussed on the upside growth and inflation risks from the fiscal boost and now see the ECB policy rate ending 2025 at c2.0%, up from c1.80% (Bloomberg, 6 March 2025).

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/eur-usd-hits-4-month-high/