like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Investment Weekly: Tracking Hormuz traffic

Key takeaways

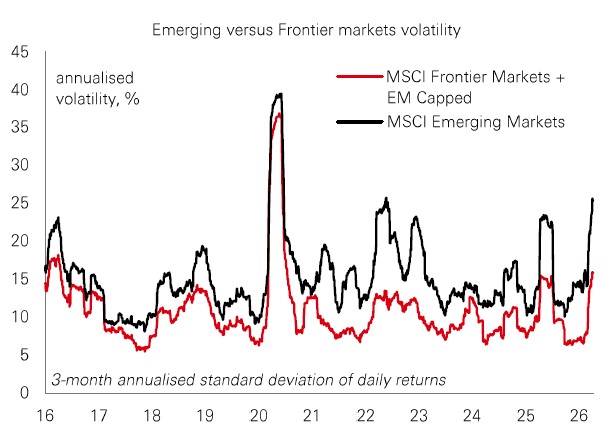

- A lot has been said about the resilience of emerging market (EM) assets during the Iran conflict so far. But what’s also been quite impressive is that the performance of frontier market stocks during this phase. The peak drawdown was limited to around 8%, versus 13% for EM.

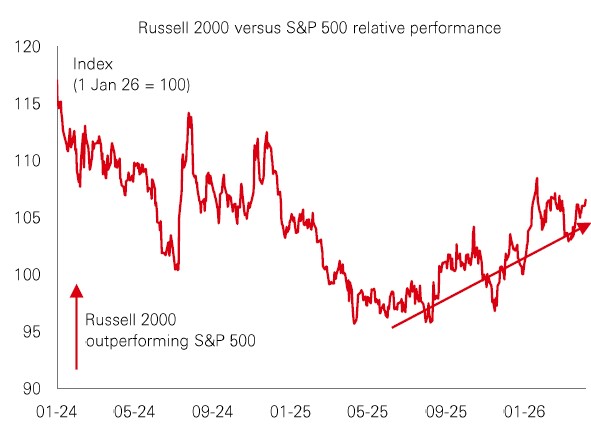

- Since last summer, the trend has been for small caps to outperform large caps, helped by expectations of more rate cuts in 2026. So, when markets repriced in a much more hawkish direction last month, it would have been reasonable to assume that small caps would be pummelled. Rather, following an initial sell-off, there was a quick bounce back.

- Last week’s sharp recovery in European stocks was unsurprising given the region’s dependency on imported energy supplies. But could Europe’s vulnerability have been overestimated in the first place?

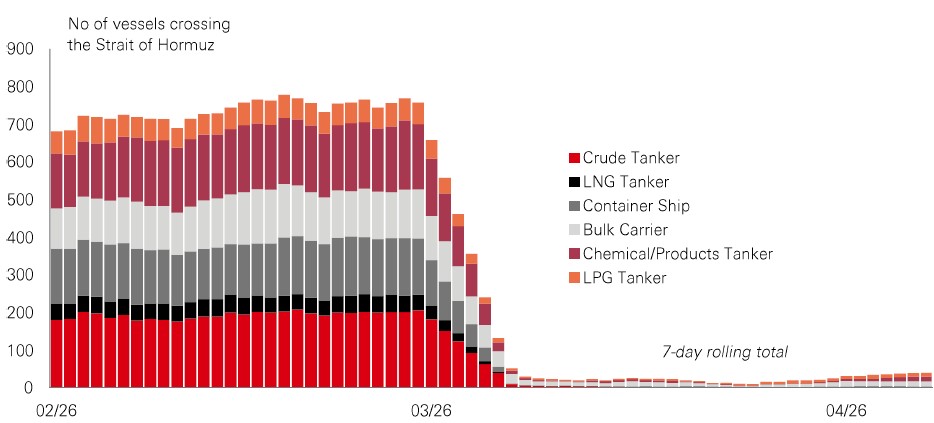

Chart of the week – Tracking Hormuz traffic

Geopolitical risk premiums compressed, and markets rallied last week after the news of the US/Iran ceasefire. But what should investors be watching now?

First, the key macro variable is how quickly vessel crossings at the Strait of Hormuz rise. The strait is a strategic chokepoint and a hinge factor for what happens next. If the data confirms a re-opening is underway and crossings are serially increasing, risk assets can continue to rally, even if other issues around the conflict remain unresolved.

Second, we look at the trend in oil prices. Brent and WTI prices have dropped back after a rapid rise, which even outpaced what we saw in the early part of the Ukraine crisis in 2022. But the spread between spot and futures prices remains elevated: around USD20 compared to 9-month ahead Brent. It takes around four days for oil tankers to reach India. If supply disruptions are progressively easing, the oil futures curve will flatten, supporting investor sentiment.

Third, it’s about policy interest rate expectations. In bond markets, traders have fretted that stagflation vibes would force rate-setters at the Bank of England and the European Central Bank to hike. Bets for Fed rate cuts later in 2026 were also taken off. But central bank watching is about both tracking the data and understanding the minds of policymakers. If the strait re-opens and oil futures curves drop, they will be more comfortable to “look through” the energy shock and not hike rates.

Market Spotlight

Chi-tech

The stellar performance of “China Tech” was a major market theme last year. And while developments in the Middle East have recently shifted investor attention, China’s technology story continues to race ahead.

The country’s recent five-year plan stressed that tech capability remains a key priority, together with boosting productivity and economic self-reliance. This reflects efforts to rebalance the economy as a solid domestic growth engine. For investors, this focus on productivity-driven expansion is showing up in the performance of Chinese stocks.

Over the past two years, the Shenzhen Chinext index – the so-called “China Nasdaq” – has seen a remarkable double-digit return. While it’s more volatile than the US Nasdaq, Chinext has outperformed its counterpart, helped by heavy exposure to advanced manufacturing, green energy and semiconductors – all sectors that domestic policy is supporting. It comes as the broader Chinese market is seeing a switch from persistent downward profits revisions to a profits-driven recovery. While last year’s performance lifted valuations, they remain moderate relative to both longer-term averages and global peers. With tech, AI and other innovation-led industries central to the market outlook, China Tech looks set to remain a major theme.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Source: HSBC Asset Management, Bloomberg, Macrobond. Data as at 7.30am UK time 10 April 2026. Asset class performance is represented by different indices. US 60/40: Bloomberg EQ:FI 60:40 Index, 10yr UST: ICE BofA 10yr US Treasury Index, Global IG: Bloomberg Barclays Global IG Total Return Index unhedged. EMD local currency: JP Morgan EMBI Global Total Return local currency. Global Equities: MSCI ACWI Net Total Return USD Index. China: MSCI China Index, India: MSCI India Index. Frontier: MSCI Frontier Markets Total Return Index. Alternatives: USD: DXY Index, Gold Spot $/OZ, Infra Equity: Dow Jones Brookfields Global Infrastructure Total Return Index, REITS Real Estate: FTSE EPRA/NAREIT Global Index TR USD. **Crypto: Bloomberg Galaxy Crypto Index. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Lens on…

The quiet achiever

A lot has been said about the resilience of emerging market (EM) assets during the Iran conflict so far. That makes sense when you think about the fundamental changes built into emerging market economies over the past few years, whether in the form of improved fiscal and external balances, or enhanced policy frameworks. But what has also been quite impressive is the performance of frontier market stocks during this phase. The peak drawdown was limited to around 8%, versus 13% for EM.

This highlights a long-standing theme when it comes to exposure to frontier market equities: they are usually less volatile. In this episode, the emerging markets index is exposed via its big weighting in Asian economies that depend heavily on gulf energy supplies, whereas key frontier markets (like Vietnam, Romania, and Kazakhstan) are less affected. Structurally, frontier markets are also insulated by a strong domestic ownership base that is less sensitive to global swings in risk appetite. A valuation discount versus EM peers also provides a natural downside buffer.

The good and the bad of broadening out

Since last summer, the trend has been for small caps to outperform large caps, helped by expectations of more rate cuts in 2026. So, when markets repriced in a much more hawkish direction last month, it would have been reasonable to assume that small caps would be pummelled. Rather, following an initial sell-off, there was a quick bounce back.

We think this reflects two aspects of the broadening-out story. First, there are the “good” attributes of small caps in the current environment. Their big domestic revenue base is a virtue in a world of higher tariffs and energy prices that make global supply chains and logistics more expensive. In the US, the small-cap index has a significant weighting in energy firms, which remain big winners from the AI and broader capex buildout.

Second, there are the “bad” vibes around the AI boom. Large-cap tech is now perceived to be capital-intensive with a lower ROI. The distribution of risks around future profits has widened, and the market is placing a premium on predictable cash flows. Overall, a mix of the “good” and the “bad” means that the broadening-out story can remain intact even in a higher-for-longer rate environment.

Substitution effects

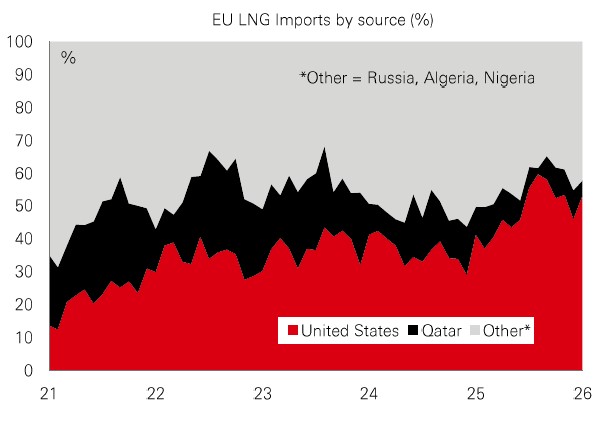

Last week’s sharp recovery in European stocks was unsurprising given the region’s dependency on imported energy supplies. But could Europe’s vulnerability have been overestimated in the first place? For starters, there has been a big push into renewables since 2022, including through REPowerEU. This has reduced dependence on gas and made electricity prices less mechanically tied to gas price spikes. Increased utility hedging has also dampened volatility.

Europe’s LNG mix has also shifted, with most imports now coming from the US. And the EU has made storage targets more flexible versus 2022, especially under unfavourable conditions such as now, reducing the risk of a panicked buyer stampede and a further spike in prices.

With the crisis less acute than it was in 2022, the overall government response to help shield consumers and businesses is also likely to be much weaker, especially with the bond vigilantes breathing down their necks. With growth more fragile than in 2022, the ECB will be under less pressure to offset the pickup in inflation. The recovery in the region’s risk assets could have further to go.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Costs may vary with fluctuations in the exchange rate. Source: HSBC Asset Management. Macrobond, Bloomberg, European Central Bank, Refinitiv. Data as at 7.30am UK time 10 April 2026.

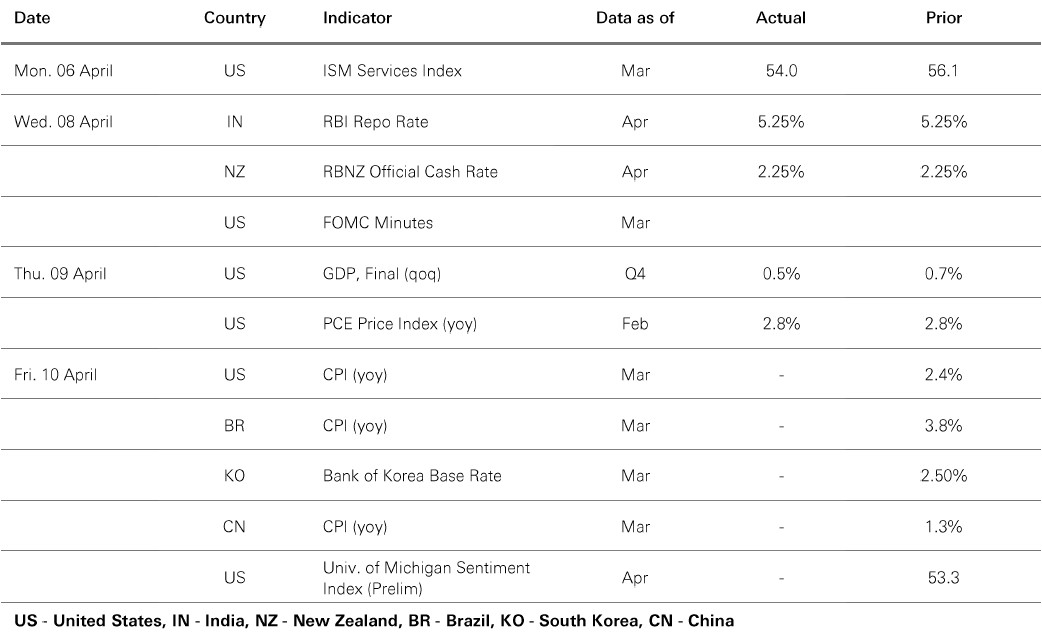

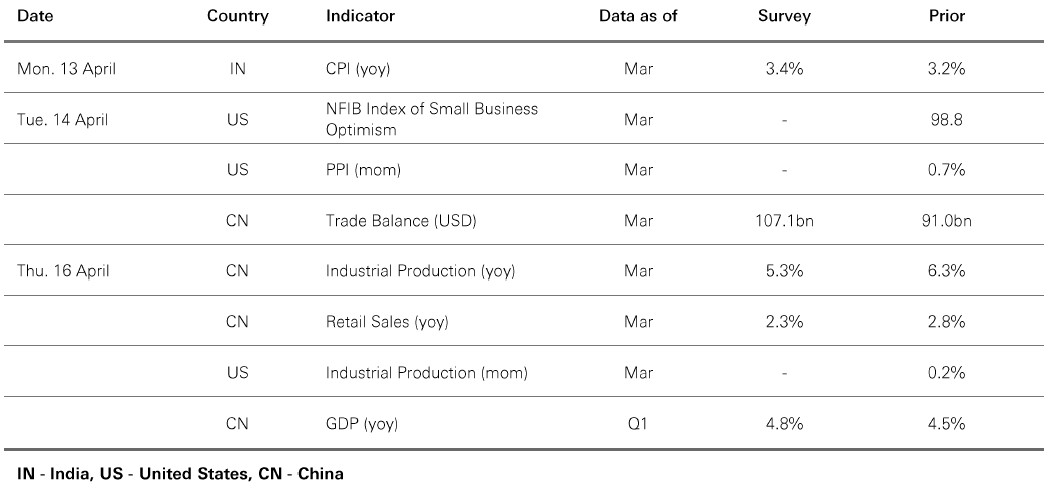

Key Events and Data Releases

Last week

The week ahead

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Source: HSBC Asset Management. Data as at 7.30am UK time 10 April 2026.

Market review

Global stocks rallied last week, as the US and Iran agreed to a two-week truce amid the ongoing Middle Eastern conflict. In developed markets, Japanese stocks led the gains. European and US indices also rallied on positive sentiment. In emerging markets, gains were broad-based, with large gains in South Korea and India. Government bonds ended a volatile week marginally higher, as sharp gains earlier in the week faded. Meanwhile, investment grade and high yield bonds strengthened. In FX, the US dollar ended lower while sterling and the euro appreciated. In oil markets, Brent crude prices were volatile but ended the week sharply lower, despite uncertainty over the credibility of the announced ceasefire. In precious metals, gold prices moved higher, reversing the previous week's declines.

https://www.hsbc.com.my/wealth/insights/asset-class-views/investment-weekly/article/