like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: Gold rally to extend into 2026

Key takeaways

- Gold prices are supported by risk aversion and a weaker USD.

- Central banks continue robust gold purchases, while Italy reviews gold reserve ownership.

- In our precious metals analyst’s view, USD softness and policy risks may sustain gold prices in 2026, but volatility is expected.

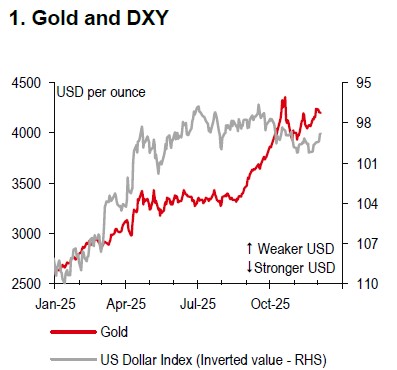

Gold prices have recently returned to around USD4,200 per ounce, underpinned by increased risk aversion and growing expectations of a 25bp rate cut by the Federal Reserve (Fed) at its 9-10 December meeting.

The recent weakness in the broad USD − reflected by the US Dollar Index (DXY) falling below 99 − has further supported gold prices, given their typically inverse relationship (Chart 1). However, with markets having largely priced in the anticipated rate cut (Bloomberg, 4 December), any subsequent decline in the USD is expected to be modest. While gold’s upward momentum remains intact, our precious metals analyst notes that a lack of improvement in physical demand may constrain further near-term gains.

Meanwhile, official sector demand for gold remains strong. The World Gold Council reports that central banks purchased a net 53 tonnes of gold in October, marking the highest monthly increase this year and a 36% rise from September. Nonetheless, potential changes are on the horizon, as the Italian government considers amending the ownership structure of central bank gold reserves. Previous attempts to transfer these reserves to the Treasury have faced resistance from EU authorities, citing Lorenzo Bini Smaghi of the Institute for European Policymaking. Italy currently holds the world’s third-largest official gold reserves, behind only the US and Germany.

Source: Bloomberg, HSBC

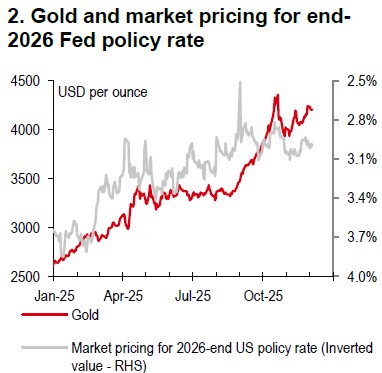

Source: Bloomberg, HSBC

Looking ahead, the appointment of the next Fed Chair, following Jerome Powell’s term ending in May 2026, will be a key factor for markets. The new appointee is unlikely to prompt a significant hawkish policy shift, keeping the USD defensive and favouring gold in 2026 (Chart 2). In addition, persistent geopolitical, fiscal, and economic policy risks are likely to sustain upward pressure on gold, although our precious metals analyst expects heightened volatility and some price moderation in 2H26 as supply-demand dynamics evolve.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/gold-rally-to-extend-into-2026/