like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Macro Monthly: Global activity on a firm footing

Key takeaways

- The rollercoaster ride for geopolitical and trade uncertainty continues, but the global macro picture remains firm…

- …even as financial markets try to second guess the policy implications of Fed Chair nominee, Kevin Warsh.

- US tariff threats abound, but few have been delivered, with the main trade news coming from US or European trade deals.

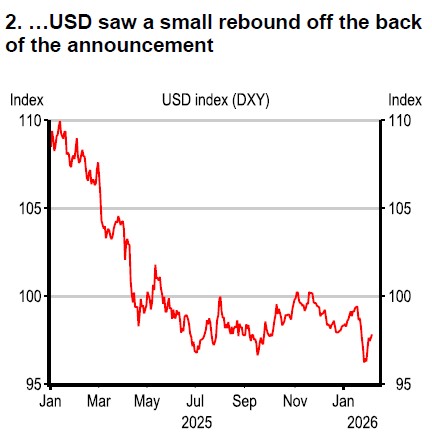

Six weeks into 2026, the twists and turns in geopolitics continue, but while they had continued to drive precious metals sharply higher for much of January, the announcement of Kevin Warsh as the next Federal Reserve (Fed) chair saw much of the early 2026 moves unwind. Currencies continue to swing around with the appreciation of the EUR raising questions for the European Central Bank (ECB) rate path, especially given January’s 1.7% inflation print. JPY bounced sharply as news of a snap election triggered FX intervention chatter.

Divergent central banks

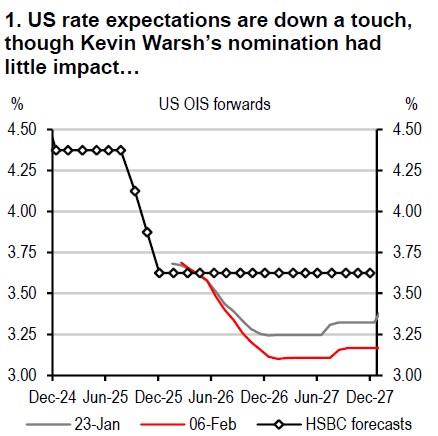

There is much discussion on potential implications for the size of the Fed’s balance sheet with Mr Warsh as Chair, but market expectations of two more Fed rate cuts in 2026 are little changed. Our forecast remains for unchanged rates given robust activity set to be bolstered further by tax cuts, inflation looking sticky, and mixed labour market signals. Other central bank action has been hugely divergent: the Reserve Bank of Australia (RBA) delivered a hawkish rate rise; Colombia a bigger-than-expected 100bp rate hike; Brazil is set to revert back to cutting in March; and the Bank of England (BoE) points to further loosening soon.

Source: Bloomberg, HSBC; Note: OIS = Overnight Index Swap

Source: Macrobond

Firm global activity

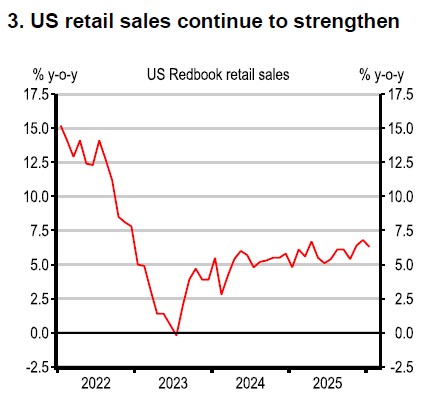

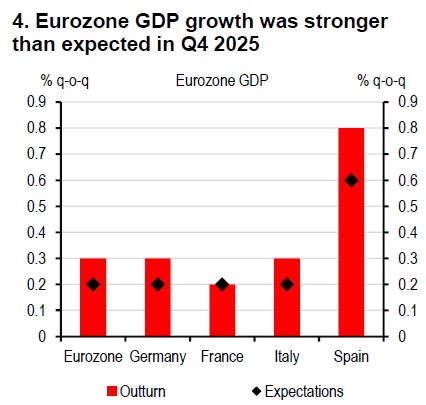

Globally, inflation is stable or slowing in many places but not all, and various input price pressures have emerged, from some key industrial metals, to memory prices, to natural gas. Global activity has stayed firm with US consumer spending, eurozone GDP and German industrial orders surprising to the upside in Q4, and global manufacturing and service sector PMIs firming in January. In Asia, mainland China GDP growth slowed in Q4, but elsewhere in the region, growth has surprised on the upside with policy generally supportive and India’s recent FY27 budget – projecting a fiscal deficit of 4.3% of GDP – represents the slowest consolidation in six years.

Source: Macrobond, Redbook

Source: Eurostat, Bloomberg

New tariffs

On the trade side, there has been no shortage of US tariff noise: US ambitions for Greenland – and associated warning of 25% tariffs on Europe – de-escalated post-Davos. Tariff threats against Canada and Korea, on any country selling oil to Cuba and – following recent protests – any country doing business with Iran, have all followed. But the only new US tariffs imposed so far this year are the 25% tariffs on a very narrow category of semiconductors and even those are lower than feared.

Trade deals

The more significant news has been the progress on bilateral trade deals both with and without the US. The EU has signed trade agreements with Mercosur and India, both pending approval by the European Parliament. Mainland China has engaged in negotiations with the UK and Canada, resulting in limited tariff agreements for both. A US-India trade deal has also been announced under which tariffs on Indian imports will fall to 18%, down from 50%.

Source: Bloomberg, HSBC

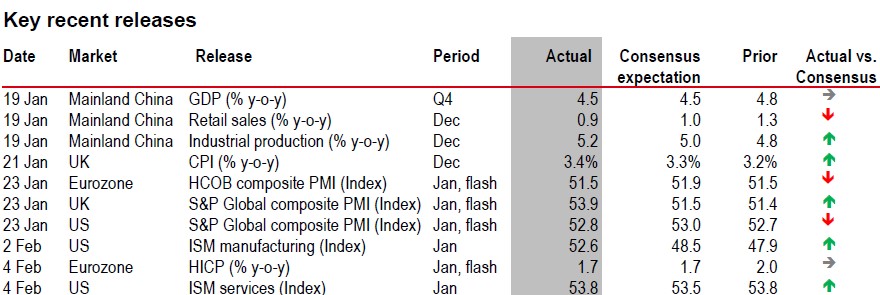

⬆ Positive surprise – actual is higher than consensus, ⬇ Negative surprise – actual is lower than consensus, ➡ Actual is in line with consensus

Source: LSEG Eikon, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/macro-monthly/global-activity-on-a-firm-footing/