like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

UK in Focus: Fragile with a hint of potential

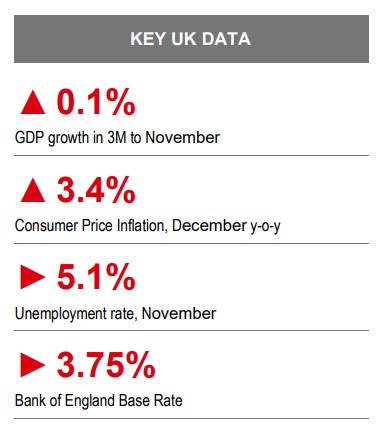

Key takeaways

- There are signs that demand is stabilising, but subdued consumer confidence points to a fragile outlook.

- Bank Rate was left unchanged at 3.75%, and although further cuts are expected…

- …the timing and scale of rate reductions is more uncertain.

Fragile with a hint of potential

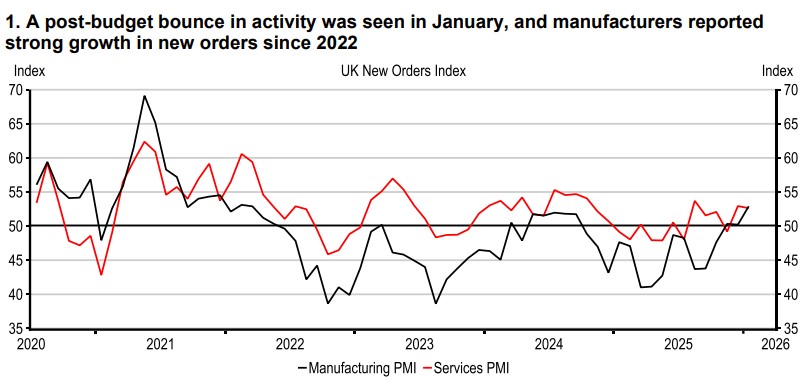

The year has started with mixed and volatile data, so it’s unclear how much underlying momentum in the economy has improved. Measures of business activity reported a sharp rebound in activity in January, most notably across services firms. However, consumer confidence ticked only 1pt higher, as improved confidence in personal finances was offset by lower expectations of the economy for this year. Those dynamics left consumers to continue to prefer saving. Elsewhere, there were signs that demand conditions are, at least, stabilising, house prices rose 0.3% m-o-m and manufacturers reported the fastest pace of new order growth since May 2022.

While the outlook is a fragile one, there is scope for a more marked improvement in demand. But we need to see a stable policy environment and a more sustained improvement in confidence to support underlying growth.

Source: HSBC

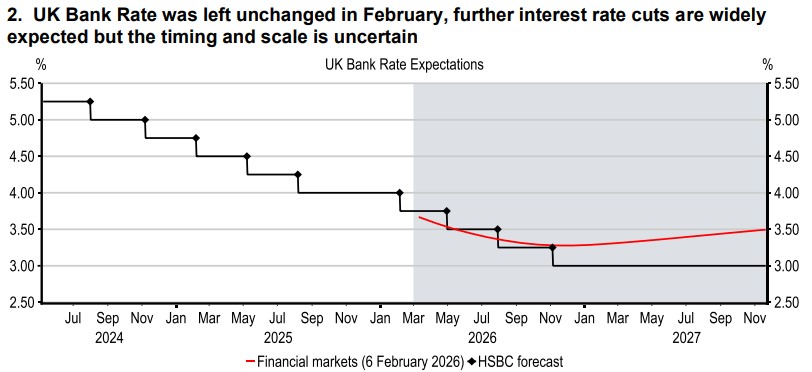

Bank of England hints at further rate cuts

At its latest policy meeting the Bank of England’s (BoE) Monetary Policy Committee left Bank Rate unchanged at 3.75%. Four of the nine-strong Committee voted for a cut, while more broadly, policymakers appear to be gaining confidence in the disinflationary process. The prospect of lower inflation reflects weak demand in the economy, a higher rate of unemployment, and policy measures announced at the Autumn Budget. Governor Andrew Bailey, who voted for unchanged rates this month, will be key in determining the timing of the next cut, given his relatively middle ground stance. Mr Bailey suggested that he needed to see a further falls in inflation expectations alongside the expected moderation in the current inflation rate. That would help to further alleviate concerns of upside risks to inflation over the medium term. It is widely expected that the CPI inflation rate will fall to around 2% in April 2026.

Then there is the question of how many more rate cuts are in prospect, and where Bank Rate may settle. That will be determined by how restrictive the Committee currently views interest rates to be on economic growth and inflation and whether any restrictiveness should remain in place for a more prolonged period. The latest BoE forecasts point to lower inflation, relative to its November forecast, and while the upside risks to inflation are judged to have diminished, they remain a source of uncertainty. Ultimately, after six rate cuts since August 2024, and with Bank Rate closer to its ‘neutral’ level, decisions on further rate cuts are likely to be finely balanced.

Source: Macrobond, S&P Global, HSBC

Source: Macrobond, Bloomberg, HSBC forecast

https://www.hsbc.com.my/wealth/insights/market-outlook/uk-in-focus/fragile-with-a-hint-of-potential/