like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

China in Focus: China anti-involution push – Stepping up a gear

Key takeaways

- There’s been plenty of talk about China’s anti-involution campaign, but so far tangible progress remains limited.

- The authorities are committed to this agenda but must balance it with other priorities like keeping the labour market stable.

- Industrial consolidation is still at an early stage: green transition, merger and acquisition activity will contribute; fair competition is key.

China data review (Jan 2026)

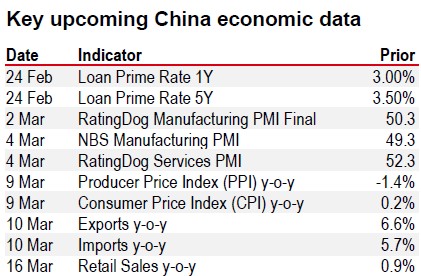

- China’s first inflation print in 2026 shows a mixed performance. CPI growth slowed to 0.2% y-o-y in January amidst a high base from last year, given distortions from the Chinese New Year (January 2025 versus February 2026). This suggests a rosier CPI figure ahead in February. Meanwhile, PPI dropped 1.4% y-o-y, but strong non-ferrous metals prices and the ongoing anti-involution campaign helped cushion the fall, with the rate of decline easing to its slowest pace since August 2024.

- China’s January NBS PMI print suggests some renewed pressure as both the manufacturing (49.3) and non-manufacturing (49.4) gauges fell back to contractionary territory after a temporary reprieve in December 2025. A key drag on the manufacturing front stemmed from new orders, which dropped to 49.2. Although recent local GDP targets indicate that China may adopt a more cautious stance for this year’s national GDP goal, this NBS reading again highlights that proactive fiscal policy and “moderately loose” monetary policy are needed to help boost domestic demand.

- China’s January credit data showed an economy that remained on a relatively weak footing as real demand stayed muted. Total Social Financing came in at RMB7.2trn in January, up 8.2% y-o-y, driven by government support, but new bank lending stayed muted at RMB4.7trn. Accelerated government bond issuance will help to kickstart projects, given that this year is the first of the 15th Five Year Plan. Household and business confidence still need more support to transmit into a broader improvement in investment this year.

China anti-involution push – Stepping up a gear

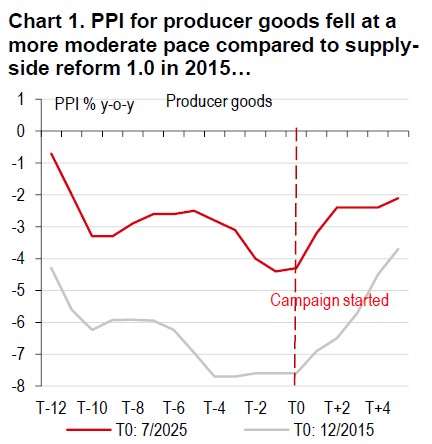

China’s anti-involution campaign was launched in July 2025 to much fanfare and was aimed at combating the intense “race-to-the-bottom” price wars and supporting sustainable industry growth. It initially worked with producer price inflation turning positive in sequential terms from October, led by a few sectors like aluminium, copper, and coking coal.

To date though, guidance has been largely advisory rather than compulsory, and included voluntary production cuts by industry associations, regulatory reforms, such as amendments to the anti-unfair competition law, and National Development and Reform Commission (NDRC) meetings on the criteria for disorderly price competition. However, in the absence of robust monitoring and enforcement mechanisms, progress in industrial consolidation and enhancements to profit margins remain limited.

The 15th FYP shows the government’s commitment

The anti-involution campaign is far more than just a slogan; Chinese authorities are working towards a unified national market and promoting fair competition. This strategic focus is highlighted in the draft of the 15th Five-Year Plan, which stresses the urgent need to curb “involutionary competition” and rebalance the economy.

Indeed, involution frequently manifests as ‘predatory’ pricing that undercuts competitors with unsustainably low prices. To address this, we expect the government to step up endorsing and enforcing competition law principles and implement further measures to restore market order, while simultaneously balancing other policy objectives, including labour market stability and sustained economic growth.

Next steps

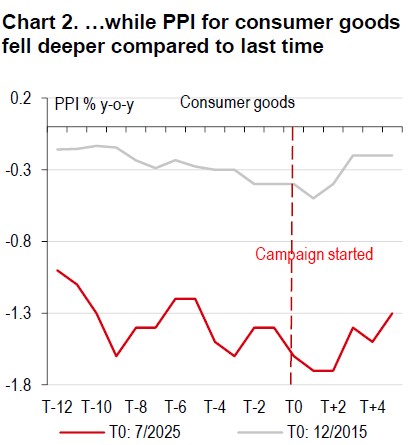

The 15th Five-Year Plan stresses the need to increase domestic consumption as a proportion of GDP, necessitating policy measures that foster sustainable consumer demand growth. Presently, the most significant deflationary pressure originates from the Producer Price Index (PPI).

Source: CEIC, HSBC

Source: CEIC, HSBC

Meanwhile, supply-side reductions are underway, and these can be complemented by targeted demand-side initiatives, particularly those with a strong pull effect on upstream sectors. For instance, infrastructure investment focused on improving human well-being and quality of life, such as better intra- and inter-regional connectivity, and expanding social housing, can effectively reflate the economy.

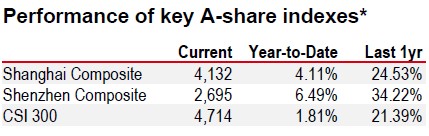

Source: LSEG Eikon

* Past performance is not an indication of future returns

Source: LSEG Eikon. As of 11 February 2026 market close

https://www.hsbc.com.my/wealth/insights/market-outlook/china-in-focus/china-anti-involution-push-stepping-up-a-gear/