like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint Flash: RMB: Managing the tempo

Key takeaways

- The PBoC will remove the 20% reserve on USD-CNY forward contracts, starting from 2 March…

- …this change is intended to moderate, not reverse, RMB appreciation, in our view.

- The RMB is likely to strengthen further against the USD, while the PBoC could relax more measures.

On 27 February, the People’s Bank of China (PBoC) announced that it would reduce the risk reserve requirement for onshore USD-CNY forward contracts from 20% to 0% from 2 March. This measure, which was reinstated on 28 September 2022 to curb RMB depreciation expectations as USD-CNY surpassed 7.00, has now been unwound.

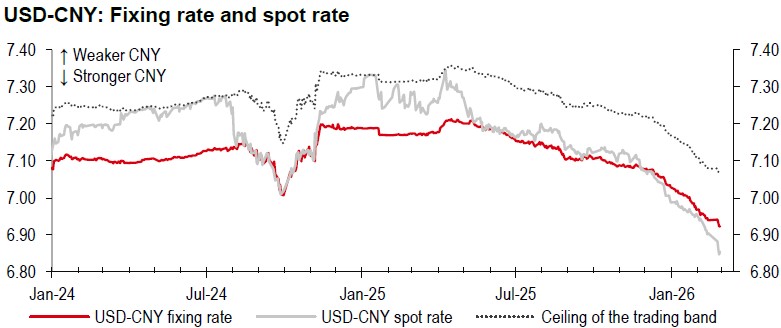

We view this adjustment not as an attempt to halt or reverse RMB appreciation, but rather to moderate its pace. Since the Lunar New Year holiday, USD-CNY fixing rates have reached new multi-year lows, and the RMB has strengthened notably against the USD. The China Foreign Exchange Trade System (CFETS) RMB Index also rose further, indicating the RMB has been strengthening against a basket of currencies. Meanwhile, the spread between the fixing and the spot rates has widened (see the chart below). Recent cross-border flows indicate that onshore corporates and investors have been selling USD at a record pace, resulting in unprecedented net short USD-CNY forward positions. In this context, the PBoC’s decision to remove the risk reserve requirement appears justified.

Source: Bloomberg, HSBC

Our outlook remains that USD-RMB could decline further as we approach key events. The National People’s Congress on 5 March is likely to focus on domestic priorities, such as industrial upgrading, technological self-reliance, growth rebalancing, and RMB internationalisation − all supportive of a stronger currency. Additionally, US President Trump’s scheduled visit to China from 31 March to 2 April signals ongoing stability in trade relations between the two countries.

Looking ahead, the PBoC may continue to relax some of the previous policy measures. Historically, the removal of the risk reserve in October 2020 was followed by further adjustments, including changes to macro-prudential assessment (MPA) parameters in late 2020 and early 2021, as well as two reserve requirement ratio hikes on FX deposits in 2021. However, these actions did not reverse the RMB’s appreciation trend against the USD at that time.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/rmb-managing-the-tempo/