like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: USD: Tariff uncertainty resurfaces

Key takeaways

- Since the US Supreme Court struck down the IEEPA tariffs, FX movements have been fairly muted.

- Negative market sentiment appears less pronounced compared to last year.

- We expect the USD to drift lower and the EUR to edge higher in the weeks ahead.

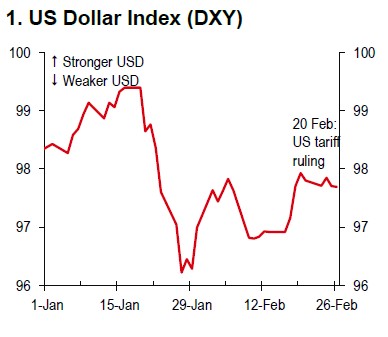

Since the US Supreme Court ruled against the Trump administration’s use of the International Emergency Economic Powers Act (IEEPA) for tariffs on 20 February, USD volatility has remained fairly muted (Chart 1). This was widely expected, given earlier signs of judicial scepticism. However, US policy uncertainty persists, especially with President Trump’s recent global tariff announcements, which could weigh on the USD and trigger market moves if major trade developments occur. That being said, the negative sentiment may not be as strong as it was after “Liberation Day” last year.

US President Trump’s State of the Union (SOTU) address on 24 February, while lengthy (a record 1 hour and 47 minutes), introduced few new policy measures. He called the Supreme Court’s decision “unfortunate” and “disappointing”, yet claimed it gives him more power to impose tariffs (Bloomberg, 24 February).

Despite these uncertainties, we are not expecting a sharp decline in the USD over the near term. Heightened geopolitical risks could, in fact, support the USD through the unwinding of short positions. The Federal Reserve (Fed) is unlikely to cut rates at its March or April meetings, a view shared by both markets and our economists, though unexpected economic data could influence future policy.

Source: Bloomberg, HSBC

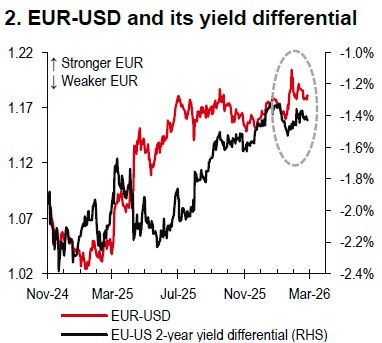

Source: Bloomberg, HSBC

EUR-USD has held steady despite ongoing EU-US trade uncertainty. The EU is likely to postpone ratification of the trade agreement as legislators seek further clarity on US trade policy (Bloomberg, 24 February). With EUR-USD trading above interest rate differentials (Chart 2), most US policy risk seems priced in. Over the near term, we expect EUR-USD to move towards the upper end of its current range, though significant new highs are unlikely. In the Eurozone, fiscal expansion and production recovery offer some upside, but a strong EUR rally would require robust wage growth or a clear credit cycle. The European Central Bank’s (ECB) influence remains limited, with no rate changes expected in 2026 (Bloomberg, 24 February).

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/usd-tariff-uncertainty-resurfaces/