like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Macro Monthly: Oil, AI & tariff uncertainty

Key takeaways

- Conflict in the Middle East caused energy prices to surge, stagflation risks to emerge, and has shaken markets…

- …at a time when the US Supreme Court’s decision to strike down IEEPA tariffs and some negative AI-related headlines…

- …had already taken the shine off what has been a pretty good start to 2026 for global growth and inflation.

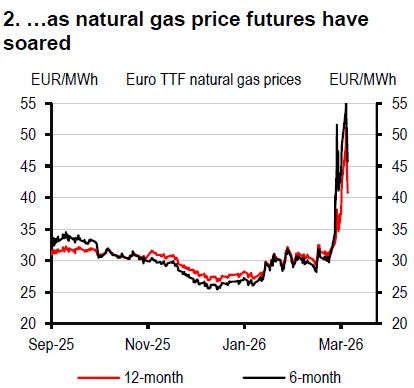

Global uncertainty surged following the effective closure of the Strait of Hormuz, through which about 20% of global crude oil and LNG transits. The reduced flow of energy trade and output caused the oil price to spike to nearly USD120/bbl until comments by President Trump that the war was “very complete, pretty much” calmed the situation.

Nonetheless, with the next stage of the conflict far from clear, the prospect of prolonged disruption to energy supplies persists. High oil and gas prices pose upside risks to inflation and monetary policy and downside risks to growth. Asian economies such as Japan, Korea, India, and mainland China source over half their energy imports from the Gulf and some have already pledged fiscal support.

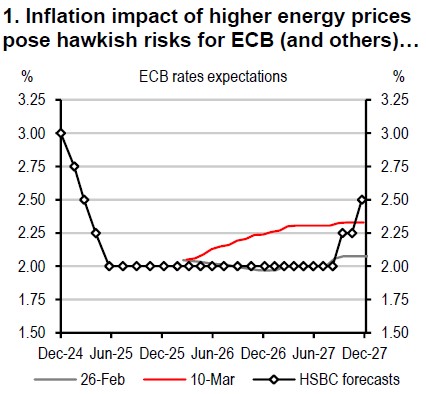

Upward pressure on interest rates

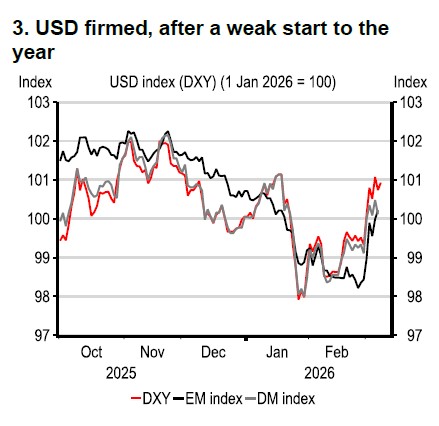

Despite the oil price easing somewhat, the hawkish repricing for the Bank of England and the European Central Bank triggered by the surge in European LNG futures has not completely reversed, and with USD having rallied, the prospects for further monetary easing by some emerging markets may have lessened too. Latam central banks are still set to see the biggest divergence ahead on policy rates.

Source: Bloomberg, HSBC forecasts

Source: Bloomberg. Latest data: 10 March. Note: TTF = Title Transfer Facility

Tariff rollback

Little more than a week before the Iran conflict began, the US Supreme Court had ruled that the Trump administration’s use of emergency powers (IEEPA) to impose tariffs on US imports was illegal. The Trump administration responded by imposing a 10% global tariff (which officials have said would be increased to 15%), benefitting some large emerging market (EM) regions, including Brazil, mainland China and Indonesia, and hitting Europe relatively harder.

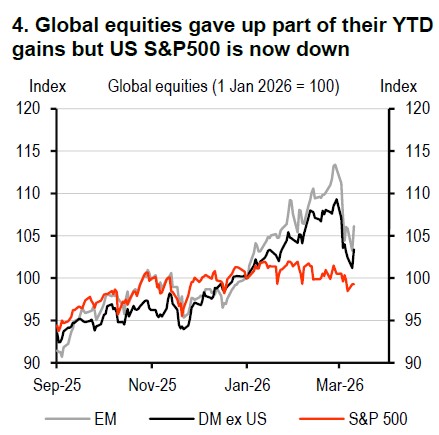

While the ruling is causing uncertainty over tariff refunds, future tariffs, and existing and future trade deals, the market reaction before the Iran conflict had stemmed from some negative AIrelated headlines, which had caused equity markets to undergo a rotation away from financials and software towards ‘real economy’ stocks.

Source: Macrobond, Latest data: 9 March. Note: EM = emerging markets, DM = developed markets

Source: Bloomberg, Latest data: 10 March Note: EM = emerging markets, DM = developed markets

Robust data

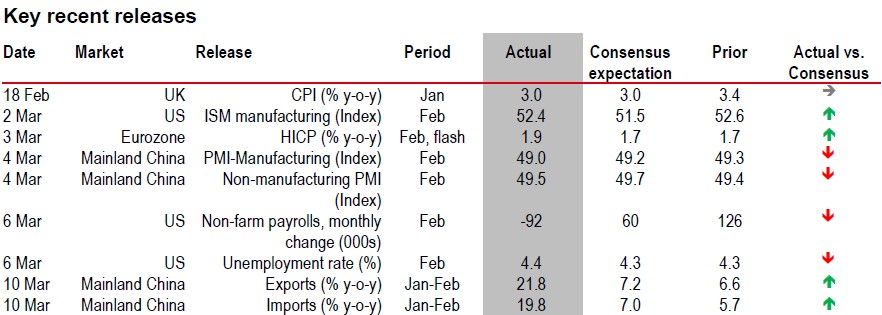

The conflict started at a time when the recent hard data had been quite solid. Global manufacturing and services PMIs (and particularly the US services ISM) increased in February even as the US labour market data continues to paint a mixed picture. January’s upside surprise in payrolls (+126k) was followed by a large drop in February (-92k) but jobless claims are low. Globally, inflation was little changed, although core inflation was up to 2.4% in the Eurozone in February and US core Personal Consumption Expenditures (PCE) was 3% in December.

In Asia, mainland China’s Jan-Feb trade data surged and attention has been on the 15th Five-Year Plan, which targets a slightly lower range of 4.5-5.0% growth for 2026, supported by fiscal policy. Policy priorities include boosting domestic demand and stepping up the anti-involution campaign, while balancing trade.

Source: Bloomberg, HSBC

⬆ Positive surprise – actual is higher than consensus, ⬇ Negative surprise – actual is lower than consensus, ➡ Actual is in line with consensus

Source: LSEG Eikon, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/oil-ai-and-tariff-uncertainty/