like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: Prolonged conflict vs de-escalation: FX implications

Key takeaways

- “Safe haven” demand has lifted the USD, but a de-escalation in geopolitical tensions will likely weaken it.

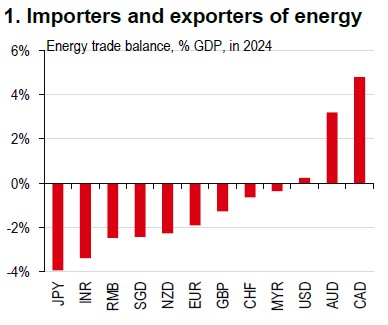

- Higher oil prices tend to weigh on currencies of large net energy importers, while the CAD and AUD look more resilient.

- A prolonged conflict could further strengthen the USD and hurt the EUR and GBP, though this is not our base case.

At the onset of the latest Middle East conflict, the USD was poised to rise, consistent with a renewed “safe haven” demand and the potential for de-risking – particularly given the build-up of sizeable, short USD positioning since January.

Higher oil and gas prices complicate the typical “safe haven” support for currencies, such as the JPY and CHF, while increasing pressure on currencies with large net energy import needs (Chart 1). In a stronger USD environment, only a narrow set of currencies, like the CAD and AUD, is likely to hold up well.

USD strength has also been accompanied by tighter US financial conditions, which is typically a headwind for other currencies. However, the tightening has been modest relative to previous stress episodes, suggesting that there may be limits to sustained USD outperformance if cross-asset volatility remains contained.

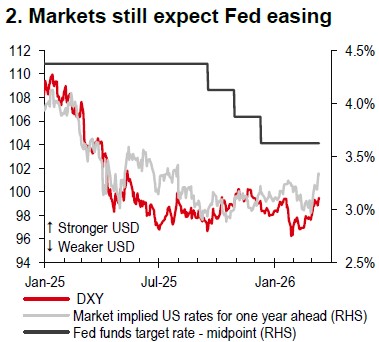

Unlike 2022, the key pillars that previously underpinned a structurally stronger USD — namely a clearly hawkish Federal Reserve (Fed) and weakening global growth — are not evident. Markets continue to price a bias towards gradual Fed easing this year (Chart 2), and leading indicators point to firmer global growth. Together, these factors can support more cyclical currencies and temper broad-based USD strength, reinforcing our central view that a de-escalation in tensions would allow the USD to resume softening. That said, risks remain skewed to the upside for the USD, if the conflict drives a sharp repricing of the Fed path into hiking territory.

Source: CEIC, UNTCAD, HSBC

Source: Bloomberg, HSBC

A further downside scenario would be a prolonged conflict that sustains energy and supply-side pressures and revives stagflationary concerns. In such an environment, the USD will likely be stronger than in our base case, supported by the US being less exposed as a net energy importer (Chart 1 again) and by growth cushioning from the One Big Beautiful Bill. By contrast, the EUR and GBP will likely underperform. While we recognise the risks associated with persistently elevated tensions and oil prices, this is not yet our central scenario.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/prolonged-conflict-vs-de-escalation-fx-implications/