like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: Most central banks wait, but the RBA hikes

Key takeaways

- Geopolitical uncertainty keeps policy and FX volatile, supporting the USD.

- The GBP may face stagflation headwinds.

- The RBA hiked again, underpinning the AUD.

FX remains closely tied to energy markets. With limited visibility on the path for energy prices, the USD is likely to stay supported as long as prices remain elevated and risk appetite fragile. However, if geopolitical risks fade, we still see scope for a reversal of much of the USD’s March strength, leaving room for a softer USD by year-end.

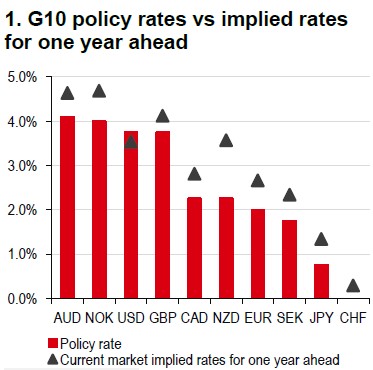

In March, many central banks chose to hold rates steady to manage heightened geopolitical uncertainty, including the Bank of Canada, the Federal Reserve (Fed), the Bank of Japan, the Swiss National Bank, the Bank of England (BoE), and the European Central Bank. Market pricing suggests that, aside from the Fed, most other G10 central banks are likely to raise rates over the next 12 months (Chart 1).

While markets lean towards a more hawkish BoE path, our economists still expect the BoE to cut rates. We also do not see energy-driven hawkishness as a durable driver of GBP strength. Instead, the UK’s stagflation risk is likely to keep the GBP under pressure vs the USD over the long term.

Meanwhile, the Reserve Bank of Australia (RBA) raised its cash rate by 25bp to 4.10% on 17 March, marking a second consecutive hike amid inflation concerns. The decision was primarily driven by domestic capacity constraints, although the Middle East conflict also contributed to upside inflation risks. The vote was narrowly split, with 5-4 in favour of the hike. RBA Governor Bullock struck a hawkish tone, framing disagreement as about timing, not the overall rate trajectory. Our economists’ central case remains that additional tightening is required, with a potential hike in May, though global uncertainty increases the risk around this call.

Source: Bloomberg, HSBC

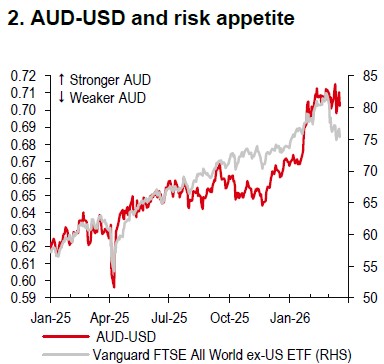

Source: Bloomberg, HSBC

Looking ahead, the AUD is likely to remain sensitive to shifts in global risk sentiment over the near term (Chart 2). The AUD may struggle to outpace the USD, but it is likely to outpace the NZD, given Australia’s strong domestic fundamentals, including a hawkish RBA stance, commodity exposure, a modest current account deficit financed largely through foreign direct investment (FDI) and portfolio inflows, and a comparatively low debt-to-GDP ratio vs other G10 economies.

https://www.hsbc.com.my/wealth/insights/fx-insights/most-central-banks-wait-but-the-rba-hikes/