like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Macro Monthly: Price shocks

Key takeaways

- Surging energy prices due to conflict in the Middle East…

- …are putting upward pressure on a wide range of prices and global inflation…

- …which could lead central banks to raise rates and consumers to pull back on spending.

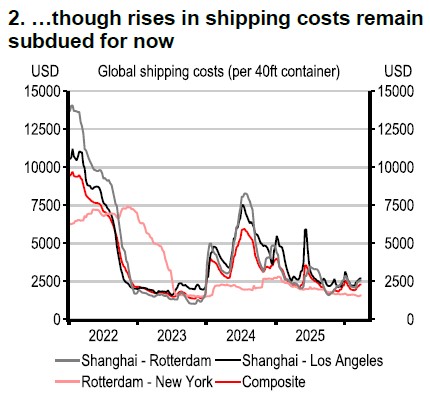

Despite the announcement of a two-week ceasefire, the global economic outlook continues to be rocked by uncertainty emanating from the Middle East – with energy prices staying elevated and worries about price shocks and shortages of a range of other commodities that come from the region, such as helium, aluminium, and some chemicals.

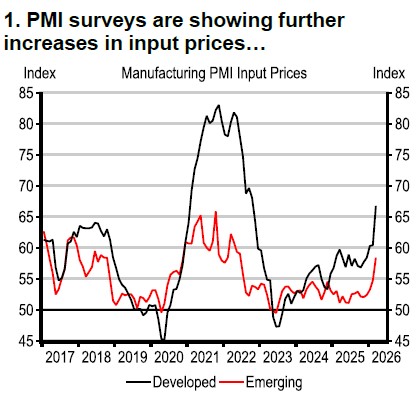

The price moves have been sharp, but the economic impact may take a few months to be fully seen. Hard economic data for March are limited, but available surveys – including PMIs and national business and consumer surveys – reflect slowing activity and widespread pricing concerns across the world.

Source: Macrobond. Latest data: March 2026

Source: Macrobond. Latest data: w/c 30 March 2026

Growth hit

The global growth-inflation trade-off has worsened – but by how much will depend on the nature and duration of the conflict, which remain highly uncertain. The impact on growth will be most acute in the Middle East, and then in Asia, where we could see much higher inflation and shortages of some materials. In Europe, we project higher inflation and weaker growth, but only see the European Central Bank and Bank of England raising rates in the more adverse scenarios.

On hold

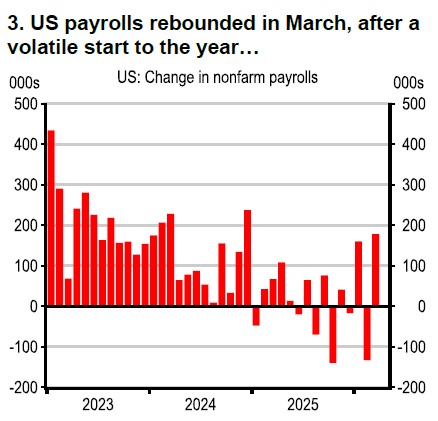

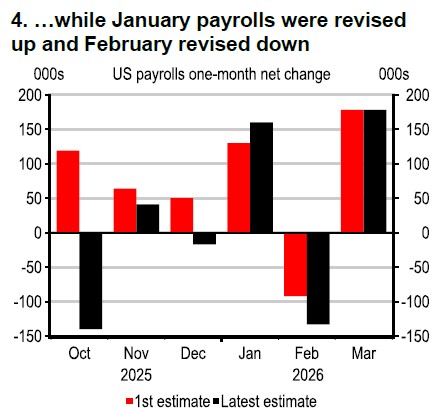

Central banks will be watching the data in the coming weeks for any signs that the energy supply shock is rippling into other parts of the global economy. Our base case is for most central banks to sit tight for now, but whilst many could be pushed into tightening, any notable rise in US unemployment could be a trigger for rate cuts. The March labour market data in the US saw a big rise in nonfarm payrolls, with the unemployment rate falling slightly, but there remain plenty of risks to the labour market outlook.

Source: Macrobond, Latest data: March 2026

Source: Macrobond, Latest data: March 2026

Inflation up

Eurozone inflation shot up in March, led by higher energy prices, but we believe that is just the beginning, with the full impact of the energy shock likely to be seen in the upcoming months. We are in a vacuum of consumer activity data – which we get with a lag – so it may be some time before we can see any impact on spending. Almost all activity data that precedes March will be of little value when thinking about the outlook.

New tariffs

On the trade front, the US announced a 100% tariff on patented pharmaceuticals on 2 April (effective in 120-180 days), yet there were significant carve-outs for generics and drugs planned to be manufactured in the US, as well as lower tariffs for the EU (among others).

Just as the global economy was turning a bit of a corner, another supply shock has derailed things. How bad it gets will depend on what happens with the conflict in the coming weeks – which is impossible to predict.

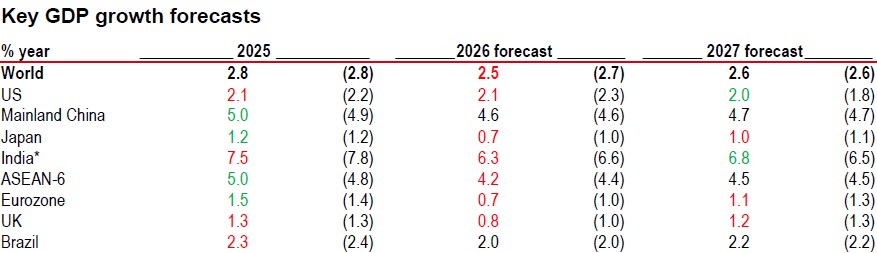

Note: *India data is calendar year forecast here for comparability. Previous forecasts are shown in parenthesis and are from the Macro Monthly dated 6 October 2025.

Green indicates an upward revision, red indicates a downward revision.

Source: Bloomberg, HSBC Economics

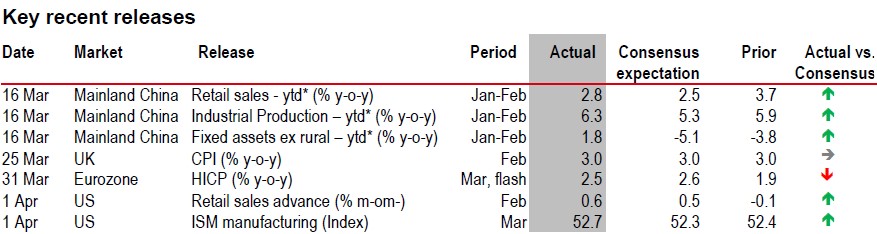

Source: Bloomberg, HSBC. * Prior numbers are for December 2025

⬆ Positive surprise – actual is higher than consensus, ⬇ Negative surprise – actual is lower than consensus, ➡ Actual is in line with consensus

Source: LSEG Datastream, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/macro-monthly/price-shocks/