like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

China in Focus: A great rebalancing

Key takeaways

- Stoking domestic demand and rebalancing trade are key priorities for China’s government this year.

- Fixed asset investment is showing signs of a recovery while manufacturing may gain from reduced tariff uncertainty.

- Fiscal and monetary measures, alongside structural reforms, are expected to support consumption.

China data review (Q1 & March 2026)

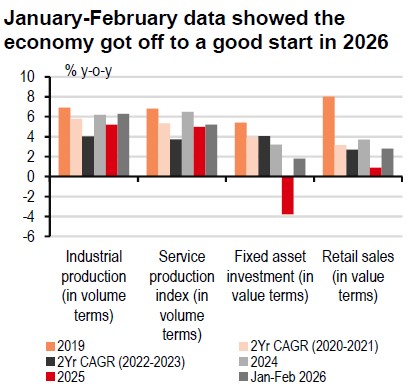

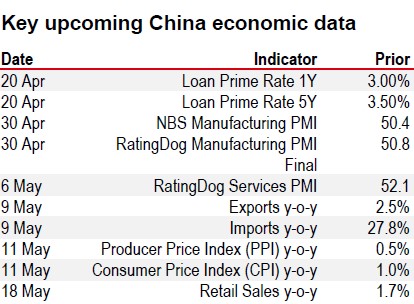

- GDP rose by 5% y-o-y in Q1, putting growth on track for this year’s government target, but global geopolitical uncertainties may still pose challenges. Growth was largely helped by outperforming exports in Jan-Feb and accelerated fiscal policy. We expect China to keep its focus on “doing one’s own thing well” with continued policy support, primarily via fiscal policy and new spending tools.

- Fixed Asset Investment rose 1.6% y-o-y in March. Infrastructure investment remained a bright spot, up 7.4%; however, property continued to drag, with overall investment falling by 11% y-o-y. Nonetheless, some property indicators improved a touch: New primary home sales by volume fell 10% y-o-y versus a 16% decline in Jan-Feb, helped by demand in tier-1 cities.

- Industrial Production rose 5.7% y-o-y in March, softer than Jan-Feb owing to lower exports in March, Chinese New Year effects and drags from the Middle East conflict. Sector data indicates resilience in electronics and transport goods, which supported the better-than-expected headline growth. This underscores China’s strong price and quality competitiveness across related sectors.

- Retail Sales slowed to 1.7% y-o-y in March, mainly weighed down by a high base and a pullback in the scale of trade-in subsidies. Auto sales (-12% y-o-y) remained the key drag as the purchase tax for new energy vehicles was adjusted from a full exemption to a 50% reduction this year. Communications appliances posted double-digit growth, remaining a structural bright spot.

- PPI returned to the positive y-o-y territory for the first time since October 2022, rising 0.5% y-o-y in March. The primary drivers were the energy and non-ferrous metals sectors along with the ongoing anti-involution campaign. On the consumer side, CPI rose 1.0% y-o-y, partly lifted by vehicle fuel prices while gold products likely also remained a key driver.

- Exports eased to 2.5% y-o-y in March amidst an unfavourable base and distortions caused by some seasonal factors. However, imports rose by 27.8% y-o-y, likely driven by domestic policy push for technological upgrading and infrastructure investment, as well as strong global AI-related demand.

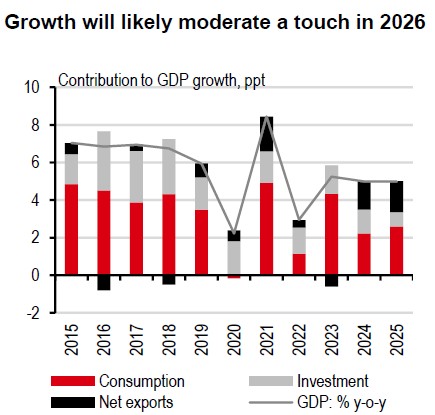

A great rebalancing

China’s 2026 growth target of 4.5-5.0% reflects a maturing economy and a strategic pivot towards sustainable, high-quality growth. The government’s focus is clear: domestic demand will be the primary engine, while there will be deliberate efforts to balance trade.

On the up

Recent data show fixed asset investment (FAI) is starting to recover after a rare contraction in 2025 across manufacturing, infrastructure, and property. The turnaround is driven by new government funding, RMB800bn in policy-related financial tools, and front-loaded bond quotas from the 2026 budget. Local governments now have more “seed capital” for infrastructure and urban development – last year’s RMB500bn unlocked RMB7trn in projects (people.com.cn, 2 November 2025), and a similar multiplier is expected this year. Ongoing local government debt swaps and repayments of local arrears should further ease liquidity pressure, boost business confidence, and attract more private capital for public projects.

Manufacturing investment stands to benefit from reduced tariff uncertainty: following recent US policy changes – including the removal of International Emergency Economic Powers Act (IEEPA) tariffs and the introduction of a Section 122 10% tariff – China’s trade-weighted tariff rate has dropped by c10 percentage points to c25%, narrowing the gap with other major exporters. Diplomatic momentum is also building: China’s foreign minister has described 2026 as a potential ‘landmark year’ for US-China relations, with up to four presidential meetings anticipated, starting with President Trump’s visit to China (South China Morning Post, 23 March 2026).

On the consumption side, support will remain robust, with another batch of RMB250bn consumer goods trade-in subsidy and a new RMB100bn fiscal-financial coordination tool to broaden support beyond goods to services and providers. Structural reforms – such as improved social welfare, pension reform, and urbanisation – are also in the pipeline to boost disposable income and raise the share of consumption in GDP over the medium term.

Trade is expected to be more balanced. As outbound direct investment grows, it will partially replace direct exports, but supply chain-related trade will expand. During the National People’s Congress in March, officials pledged to “balance trade” and expand imports, e.g., agricultural products, premium consumer goods, and advanced equipment and key components (Gov.cn, 7 March). The government’s commitment to further opening-up, especially in services sectors, should help reduce frictions.

Source: Wind, HSBC

Source: Wind, HSBC

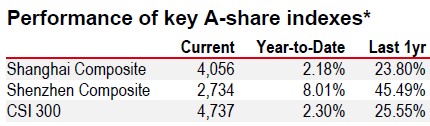

Source: LSEG Eikon

* Past performance is not an indication of future returns

Source: LSEG Eikon. As of 16 April 2026, market close

https://www.hsbc.com.my/wealth/insights/market-outlook/china-in-focus/a-great-rebalancing/