like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Investment Weekly: Magnificent margins

Key takeaways

- The US dollar has strengthened since the first Federal Reserve meeting under Chair Kevin Warsh, highlighting near-term headwinds to the widely held “dollar down” view.

- Recent data continue to point to a two-speed economy in China. On one hand, AI-tech, new energy, and advanced manufacturing are leading export competitiveness and industrial strength, keeping growth resilient. But, on the other hand, non-tech and “old economy” sectors are lagging.

- It has been a week of big political announcements in the UK. But one good news story is that the country’s productivity could be improving. But not everyone agrees.

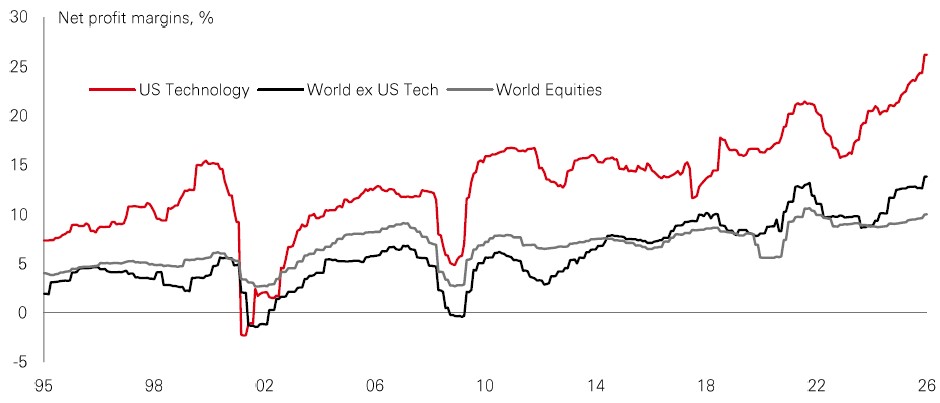

Chart of the week – Magnificent margins

Last week’s sell-off in AI-focused technology stocks has revived questions about the durability of margins and the rising cost of the AI buildout. When it comes to tech profits, there are three factors that investors should consider:

#1. Profits are powering enthusiasm – and reopening the IPO window. Today’s tech ecosystem is generating far more profit than the wider market – reminiscent of the 1990s, but even more powerful. High profits fill investors with confidence and support appetite for IPOs. Markets are already anticipating more mega-cap and smaller listings in 2026. While the opportunity can be compelling – and trigger fear of missing out – it’s important to have realistic expectations.

#2. Today’s profits are being amplified as generous tax incentives (OBBBA) and the AI arms race pull forward capex. This is creating bottlenecks and sharp price increases, with tech net margins at new highs of nearly 27%. These levels are rare: roughly double early-2000s levels and almost triple the long-run global tech average. A key driver is mammoth capex, given that around 40-45% of capex spending cycles back into the wider tech sector. But capex is lumpier than mainstream earnings, so investors are right to question their longevity.

#3. Above-average profits may offer limited upside. History is a reminder: in 1999/2000, tech profits surged relative to the market. They rolled over on the realisation that capacity exceeded end-demand. For profits to be durable, capex discipline and end-demand need to keep pace.

Overall, the tech opportunity is genuine. However, valuation discipline, diversification, and selective stock-picking remain important.

Market Spotlight

Concrete, cables, and cashflows

Infrastructure stocks – the firms that build and operate essential assets, from energy and transport networks to the AI buildout – got off to a strong start in 2026. They benefitted from a rotation away from high-growth tech into energy, utilities, and other defensive areas. While global equities have since narrowed the gap, infrastructure’s income appeal has quietly strengthened. The sector currently yields around 3.8%, and the yield spread versus broader stocks currently sits near the upper end of its 10-year range.

So, what’s the appeal? First, infrastructure cashflows tend to be resilient. Many assets earn regulated or contracted revenues that are inflation-linked, which can be attractive amid spiky inflation and potentially higher-for-longer rates. Second, infrastructure can play defence. In volatile markets, it can act as a stabiliser: it’s underrepresented in major equity indices, and correlations have been trending lower. Third, the long-term tailwinds are hard to ignore: digitalisation, electrification and deglobalisation are multi-year forces that support sustained investment.

Overall, infrastructure offers an unusual mix – yield, inflation sensitivity, and structural growth – making it a source of diversified income and portfolio resilience.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. The level of yield is not guaranteed and may rise or fall in the future. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Source: HSBC Asset Management, Factset, Bloomberg, Macrobond. Data as at 7.30am UK time 26 June 2026.

Lens on…

Dollar detour

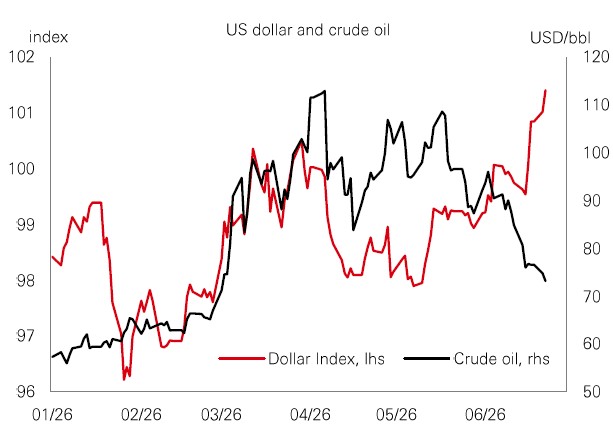

The US dollar has strengthened since the first Federal Reserve meeting under Chair Kevin Warsh, highlighting near-term headwinds to the widely held “dollar down” view.

US data continue to point to firm labour markets, with inflation proving more persistent than many expected. Markets took the Fed’s emphasis on price stability as a signal that policymakers remain willing to tighten if needed. Investors have therefore priced a more hawkish path, with consensus now expecting one Fed hike before the end of 2026. That shift has supported the dollar, reinforced by doubts over how far other central banks – especially in Europe – can keep tightening amid weaker growth.

There is an important nuance. A sharp fall in oil prices, as seen last week, would normally weaken the dollar by easing inflation fears and reducing the perceived need for tighter policy. Instead, the dollar has strengthened, suggesting that markets are prioritising the risk of further Fed tightening over the improved inflation outlook.

From bricks to bytes

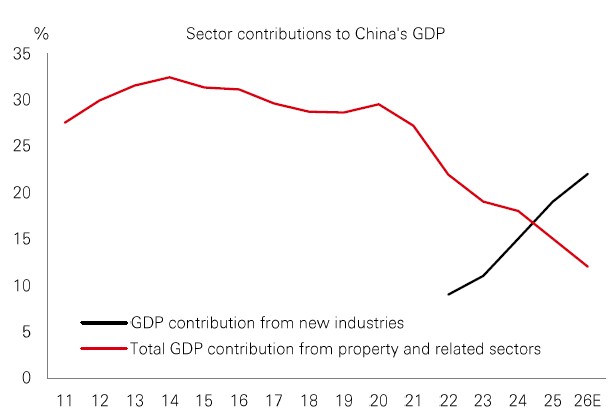

Recent data continue to point to a two-speed economy in China. On one hand, AI-tech, new energy, and advanced manufacturing are leading export competitiveness and industrial strength, keeping growth resilient. But, on the other hand, non-tech and “old economy” sectors are lagging.

This split reflects a bigger structural shift: away from credit-intensive, property- and low-cost manufacturing-led growth, towards a model powered by tech innovation. It also highlights a strategic shift in national priorities centred on self-sufficiency in the advanced tech supply-chain, and global leadership in setting tech standards.

For Chinese stocks, this macro split is translating into wider dispersion, with Technology and Materials expected to lead profits growth in 2026–2027. Some equity experts see opportunities in AI localisation, biotech breakthroughs, and upstream plays. Meanwhile, a higher weighting of “new economy” sectors in China’s onshore and offshore indices could boost overall index profitability, which together with undemanding valuations, could drive further performance.

Problematic productivity

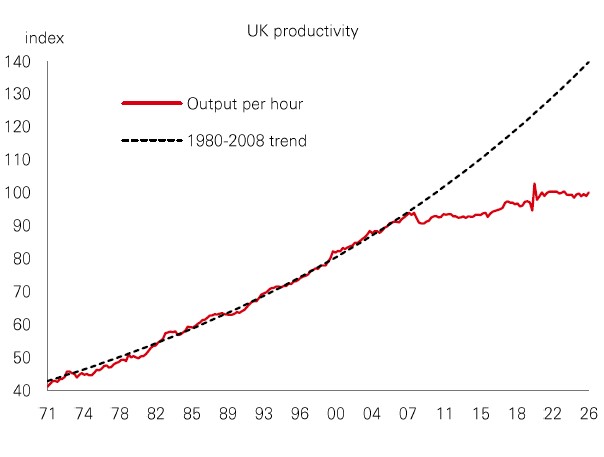

It has been a week of big political announcements in the UK. But one good news story is that the country’s productivity could be improving.

UK output has remained stubbornly below its long-term trend since the global financial crisis. But research by academic John Van Reenen suggests that this could be changing. His study of government-collected employment data found output-per-hour has picked-up since the end of 2023. He credits this to fiscal stability, higher public capital investment, and structural reforms. AI could also be a tailwind, helped by the UK’s favourable knowledge-intensive, services-led, and export-oriented mix.

But not everyone agrees. Economist and former Bank of England MPC member Michael Saunders reckons the productivity uplift is flattered by falling employment and residual seasonality. He believes gains are skewed towards lower-paid sectors, while cyclical areas like manufacturing and ICT are lagging, in part because of higher labour costs.

A tech-led upswing could be a macro boost. And while higher productivity alongside weak jobs growth is unlikely to improve living standards, it could support corporate profitability in some targeted areas of the UK economy.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Costs may vary with fluctuations in the exchange rate. Source: HSBC Asset Management. Macrobond, Bloomberg, Refinitiv, Factset. Data as at 7.30am UK time 26 June 2026.

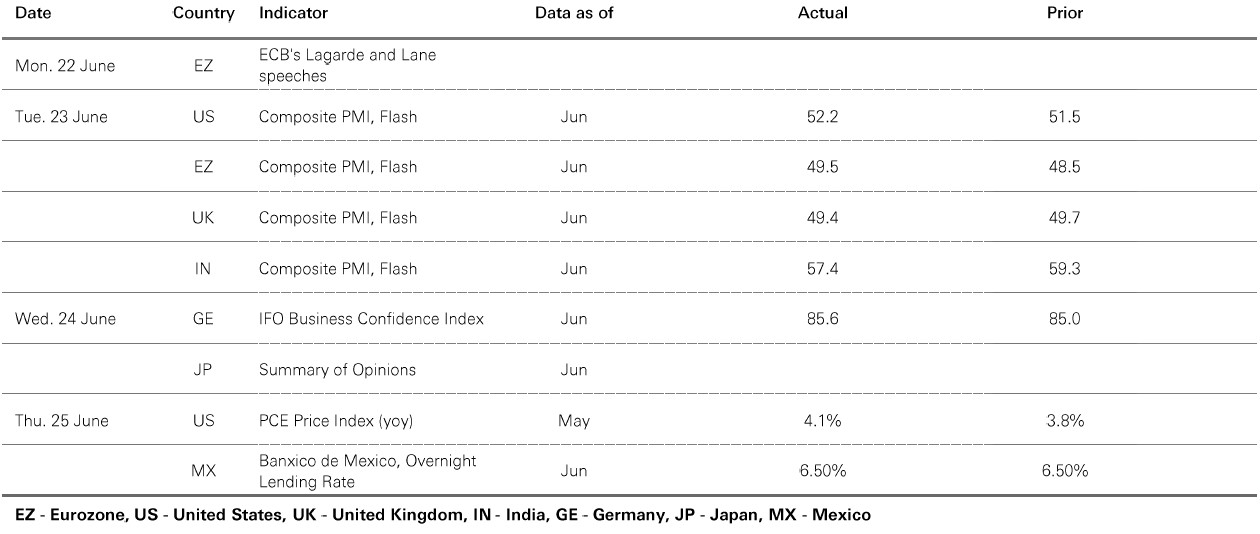

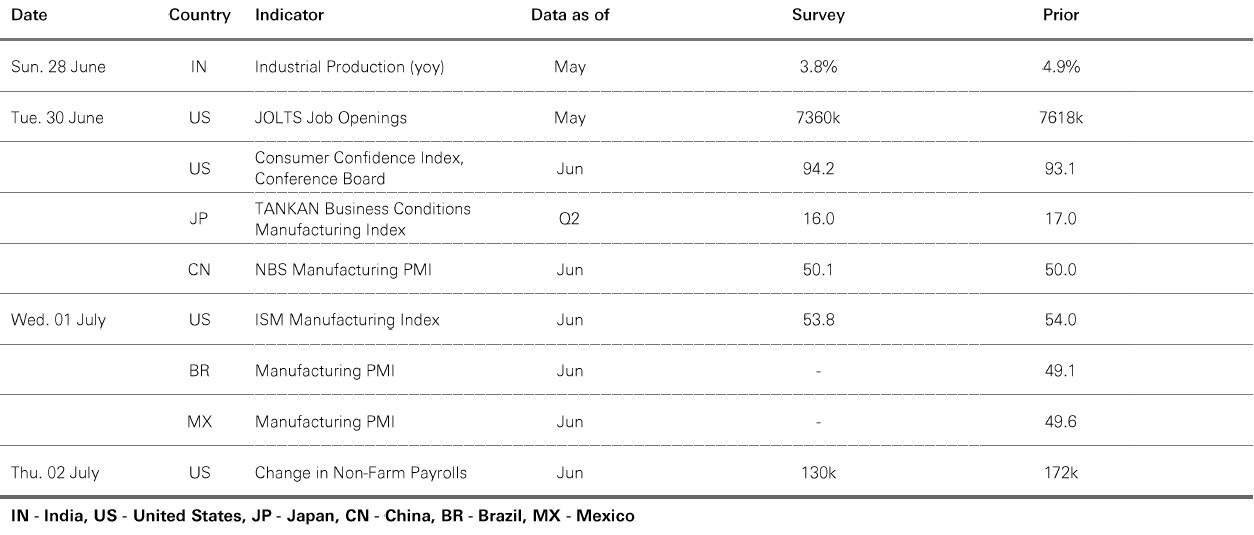

Key Events and Data Releases

Last week

This week

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Source: HSBC Asset Management. Data as at 7.30am UK time 26 June 2026.

Market review

Equities got off to a volatile start amid a global tech sell-off. US indices were mixed, with the Nasdaq Composite and the Magnificent Seven hit harder. Declines also spread across Asia’s tech-heavy markets, including South Korea, while the Nikkei 225 also fell. European exchanges were broadly positive, with the FTSE 100 outperforming. Oil prices fell further, back to pre-US-Iran tension escalation levels last seen in early March, pushing sovereign bond yields lower. The US Treasury yield curve flattened modestly, and UK gilt yields fell on domestic political news. The US dollar strengthened modestly against a basket of major currencies, while gold extended its decline, briefly falling below USD 4,000 an ounce for the first time since November.

https://www.hsbc.com.my/wealth/insights/asset-class-views/investment-weekly/