like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: EUR and JPY: Underperformance risks?

Key takeaways

- Month-to-date, the JPY has been the weakest G10 currency, and the EUR has also underperformed.

- Our base case remains for USD-JPY to move lower by yearend, but we see potential upside risks over the near term.

- If energy-related disruptions continue and Eurozone activity weakens further, the EUR is likely to face downside risks.

FX markets are likely to remain sensitive to geopolitical developments. Escalating Middle East tensions typically support the USD, while de-escalation tends to weigh on it. Within the G10, the JPY has been the weakest currency month-to-date, with the EUR not far behind (Bloomberg, 23 April).

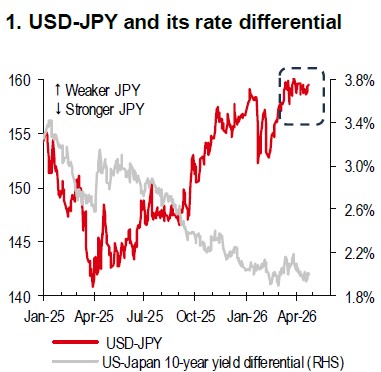

Bearish sentiment towards JPY is consistent with Japan’s macro exposure. Japan is the largest net energy importer among advanced economies (scaled by GDP) and has deep economic ties with the Gulf region. Despite these headwinds, USD-JPY has traded in an unusually narrow range recently. A cautious Bank of Japan (BoJ) and domestic fiscal challenges may delay USD-JPY’s convergence lower towards levels implied by rate differentials (Chart 1). Key fiscal watchpoints include the possibility that funding for fuel subsidies may run out in mid/late May and that a supplementary budget may be proposed.

Offsetting factors include net portfolio inflows (foreign buying of Japanese equities and bonds month-to-date in April, alongside Japanese selling of foreign bonds) and firm verbal intervention from the Ministry of Finance (Katayama: “bold action”; Bloomberg, 17 April), may help cap USD-JPY.

Our base case remains for USD-JPY to decline by year-end. Near-term upside risks include a more dovish BoJ, a more hawkish Federal Reserve (Fed), escalation in the Middle East conflict and renewed oil-price highs, and further fiscal slippage in Japan.

Source: Bloomberg, HSBC

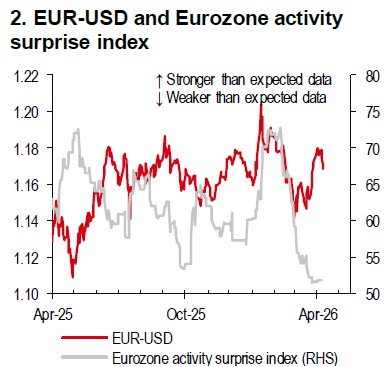

Source: Bloomberg, HSBC

Turning to the EUR, Middle East developments have been the key driver, but cyclical factors (such as growth, inflation, and policy response) are likely to determine the magnitude of moves. Eurozone flash composite PMI disappointed in April, with the private sector returning to contraction for the first time since December 2024. Price components also point to a stagflationary impulse. If disruption around the Strait of Hormuz persists, the negative impact on Eurozone growth and inflation is likely to intensify, undermining the EUR (Chart 2).

https://www.hsbc.com.my/wealth/insights/fx-insights/eur-and-jpy-underperformance-risks/