like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint Flash: JPY: FX Intervention?

Key takeaways

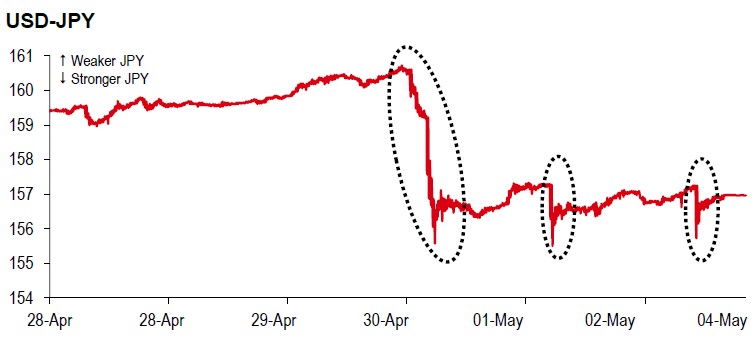

- USD-JPY fell sharply after briefly moving above 160.

- Experience from 2024 suggests USD-JPY may rebound once the initial impact fades.

- A more durable yen recovery will likely require stronger fundamentals, including BoJ rate hikes and lower oil prices.

After USD-JPY briefly moved above 160 on the evening of 30 April (JST), the pair fell sharply. It then saw two further, smaller sudden drops on 1 May (late afternoon) and 4 May (midday), both starting near 157.25 (see the chart below).

Source: Bloomberg, HSBC

Japan’s Ministry of Finance (MoF) has not confirmed any FX intervention and has kept its comments deliberately unclear, which is typical (the last clear confirmation was 22 September 2022). As a result, markets often look to the Bank of Japan’s (BoJ) daily current account data, notably “Treasury funds”, to gauge potential activity, typically with a one-day delay. Estimates suggest cJPY5.4trn (cUSD34.5bn sold; Bloomberg, 1 May) may have been used on 30 April. The MoF is due to publish the total intervention amount for 28 April–27 May on 29 May, followed by a detailed daily breakdown for 2Q26 in early July.

Will USD-JPY stay below 160?

Experience from 2024 suggests USD-JPY can rebound soon after FX intervention unless fundamentals improve. In 2024, USD-JPY began rising only days after the 29 April (~160) and 1 May (~158) interventions. It moved above 158 on 14 June after a dovish BoJ meeting, then broke above 160 on 26 June. MoF intervened again on 11 July (~161) and 12 July (~159). USD-JPY fell below 150 after a rate hike by the BoJ and a dovish hold by the Federal Reserve (Fed) on 31 July.

In our view, two factors are particularly important: (1) BoJ policy: the next decision is 16 June, with c65% chance of a 25bp rate hike expected by markets (Bloomberg, 4 May). (2) External support: in 2024, weaker US data and a dovish Fed helped; and lower oil prices may be the key driver now.

Longer-term support for the JPY would likely require a more hawkish BoJ, continued fiscal discipline, and measures to improve FX flow dynamics. Our base case is that USD-JPY may not trend materially lower, but it should be capped near term by intervention risk, with lower oil prices potentially helping over time.

https://www.hsbc.com.my/wealth/insights/fx-insights/jpy-fx-intervention/