like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Macro Monthly: Inflation reawakens

Key takeaways

- Despite ongoing peace talks, traffic through the Strait of Hormuz has yet to pick up…

- …meaning the risk of shortages is rising and energy prices are staying elevated…

- …rippling into inflation data, and eventually into growth.

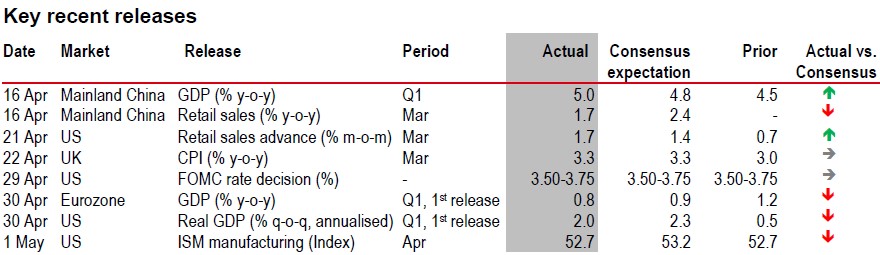

The Middle East conflict has now dragged on for more than two months, and the ripples into the global economy continue to build. The US is maintaining a naval blockade in the Strait of Hormuz, and traffic remains limited. Equity markets have recovered, but bond markets are still pointing to higher rates in the coming months.

Clearer impacts

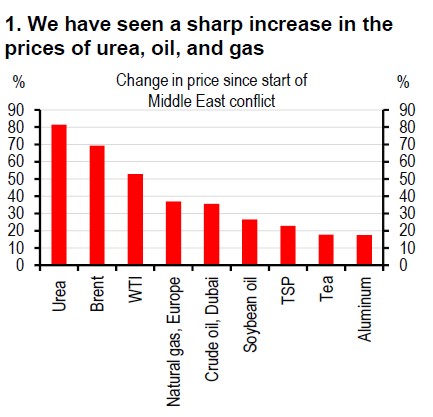

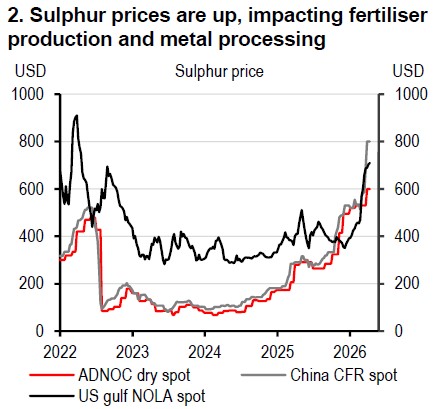

That said, the economic impact is starting to be clearer. Oil and gas prices remain high and volatile, while Asian economies, such as India, Thailand, and the Philippines, are seeing government policy focusing on limiting energy usage. It’s not just energy, either. Prices for a range of commodities, including fertilisers, urea, sulphur, aluminium, and copper, are also rising, which is making life harder for both industry and consumers. For now, much of this is in supply chains, but the risks are clear for filtering through into consumer prices as well.

Source: World Bank. Latest data April 2026. Note: TSP = Triple Superphosphate

Source: Bloomberg. Latest data 17 April. Note: ADNOC = Abu Dhabi National Oil Company; NOLA = New Orleans, Louisiana; CFR = Cost and Freight

Some of this is already showing up in the CPI data. March and April CPI prints point to a sharp rise in headline inflation, driven by higher energy costs. While some countries are providing fiscal support for retail energy prices, that is not an easy lever for policymakers to pull, especially with public debt already high.

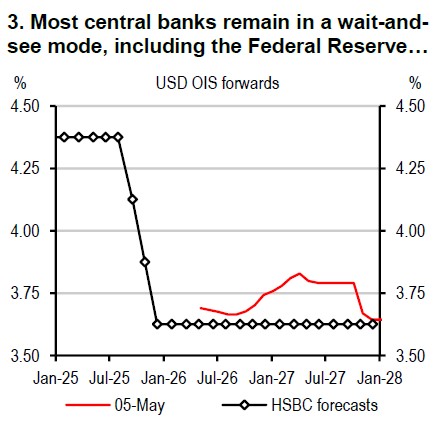

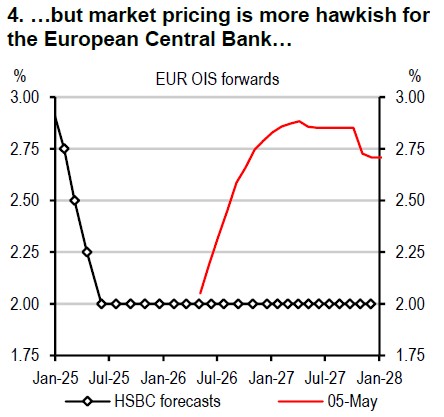

On hold

All of this complicates the policy mix. With fiscal ammunition more limited, central banks are largely in a wait-and-see mode. Higher price pressures have taken rate cuts off the table for now, but rate hikes also look unlikely in most economies, given that this kind of price shock is likely to weigh on activity as well.

Source: Bloomberg. Latest data: 5 May 2026. Note: OIS = overnight index swap

Source: Bloomberg. Latest data: 5 May 2026

The growth impact may take some time to be seen. In the US, Q1 GDP accelerated to 2.0% q-o-q (annualised), partly reflecting a rebound in government expenditure after the government shutdown in Q4 2025 and strong AI-driven investment. In Asia, Q1 GDP in mainland China surprised to the upside, while eurozone GDP saw a slowdown.

Price hikes

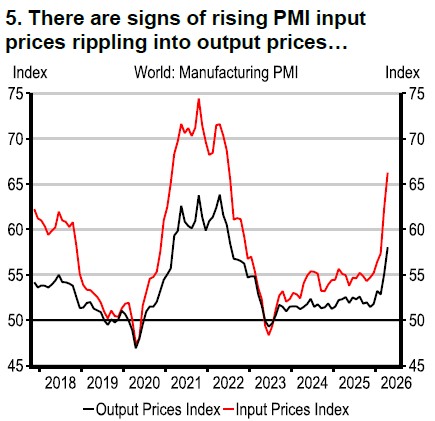

However, the PMI surveys, our first tell on the global data, are painting a painful picture of what is to come. While we may have seen some better headline data on the manufacturing front, services PMI data have been much softer. Pricing indices are up across the board, and it may take time for the inflationary shock to filter through to household and business decisionmaking, and with it, the hard economic data on inflation and activity.

The risk is, however, that the longer the Strait of Hormuz is closed, the greater the chance of acute shortages or price shocks – something the global economy is ill-prepared for.

Source: S&P Global Latest data:April 2026

Source: S&P Global Latest data:April 2026

Source: Bloomberg, HSBC.

⬆ Positive surprise – actual is higher than consensus, ⬇ Negative surprise – actual is lower than consensus, ➡ Actual is in line with consensus

Source: LSEG Eikon, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/macro-monthly/inflation-reawakens/