like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: “Risk-on” rally, but questions remain

Key takeaways

- “Risk-on” currencies gained notably against the USD amid improved market sentiment.

- Rate hikes may also have supported the AUD and NOK.

- In our view, a sustained JPY recovery likely needs stronger fundamentals beyond FX intervention.

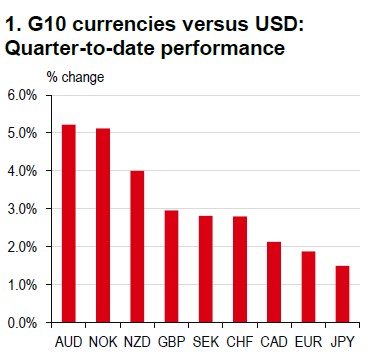

So far this quarter, “risk-on” G10 currencies, such as the AUD, NOK, and NZD have outperformed against the USD (Chart 1), helped by renewed optimism around a potential de-escalation of tensions in the Middle East.

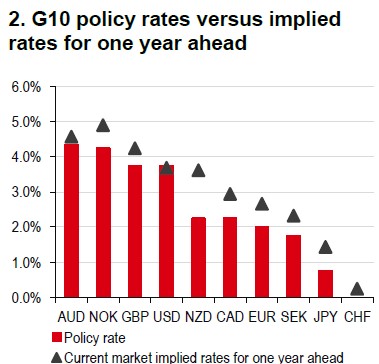

In addition to the broader shift in risk appetite, both the AUD and NOK appear to have benefited from domestic policy developments. On 5 May, the Reserve Bank of Australia (RBA) delivered a third consecutive 25bp rate hike, taking the policy rate to 4.35%, in line with market expectations. This keeps the RBA an outlier among G10 central banks (Chart 2). Our economists expect the RBA to remain on hold in a “wait-and-see” mode; however, further domestic fiscal support could increase the likelihood of additional tightening.

Data as of 7 May 2026 at 18:00 HKT

Source: Bloomberg, HSBC

Source: Bloomberg, HSBC

The Norges Bank surprised markets on 7 May by raising its policy rate by 25bp to 4.25%, marking its first hike since 2023. As the Norwegian central bank indicated that its policy outlook has not changed materially, our economists view a prolonged hiking cycle as unlikely. In contrast, regional peers, including the European Central Bank, the Bank of England and the Riksbank, still adopt a wait-and-see approach.

While recent price action is broadly consistent with these developments, it is important to monitor any sustained energy disruption that could trigger a renewed “risk-off” shift and strengthen the USD.

Meanwhile, the JPY has been among the weakest G10 performers quarter-todate (marginally ahead of the USD), despite potential support from FX intervention. While neither Japan’s Ministry of Finance nor the Bank of Japan (BoJ) has confirmed any recent action, we believe USD-JPY may stay capped over the near term. That being said, a more durable JPY recovery will likely require stronger underlying fundamentals, most notably further BoJ rate hikes and lower oil prices (see FX Viewpoint Flash – JPY: FX Intervention? for details).

https://www.hsbc.com.my/wealth/insights/fx-insights/risk-on-rally-but-questions-remain/