like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: GBP: Resilient, but two key risks

Key takeaways

- The GBP has remained resilient within its one-year range despite multiple market shocks.

- Cyclical support should persist, though further GBP upside may be capped by current market pricing.

- Key downside risks are a prolonged closure of the Strait of Hormuz and any credible weakening of UK fiscal discipline.

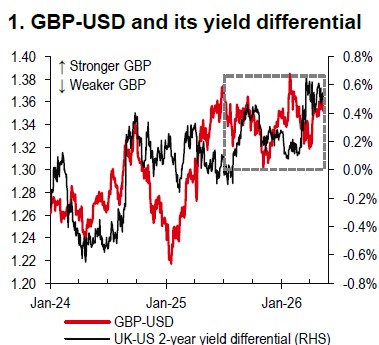

The GBP has remained relatively steady, with GBP-USD trading within its 1-year range (Chart 1) even as markets faced several shocks. This resilience has been supported by a mix of stronger global risk sentiment, favourable interest rate differentials (Chart 1 again), and tighter GBP liquidity conditions via the Bank of England’s (BoE) balance sheet reduction, even as geopolitical and UK political risks have continued to build.

Geopolitical developments in the Middle East have been a key test. While GBPUSD has held up so far, uncertainty remains, particularly around the risk of disruption to Gulf commodity supplies. A prolonged closure of the Strait of Hormuz could trigger a broader move into “safe-haven” assets, likely supporting the USD and putting downward pressure on the GBP.

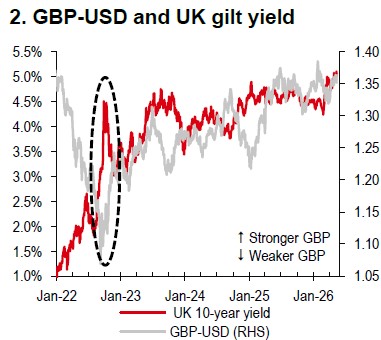

Domestically, political uncertainty has also resurfaced, with Prime Minister Sir Keir Starmer reportedly facing increasing pressure from within the Labour Party (The Times, 12 May). Confidence in the GBP remains closely tied to perceptions of UK fiscal discipline. The last major loss of fiscal credibility, in Autumn 2022, coincided with a sharp rise in UK government bond yields and a marked fall in the GBP (Chart 2), prompting temporary BoE intervention in the gilt market. If credible leadership contenders were to signal a willingness to loosen fiscal discipline, the GBP is likely to come under renewed pressure.

Source: Bloomberg, HSBC

Source: Bloomberg, HSBC

Overall, the two most important risks that could undermine the GBP’s resilience are: (1) an extended closure of the Strait of Hormuz, and (2) any credible shift away from UK fiscal discipline. Even so, we expect the GBP to remain supported through the rest of the year by cyclical drivers, particularly the BoE’s tightening bias, with our economists forecasting two 25bp rate increases in July and September. However, the scope for further GBP appreciation may be limited, as a sizeable portion of this tightening outlook is already reflected in market pricing. In fact, markets are pricing at least two BoE rate hikes by end-2026 (Bloomberg, 14 May).

https://www.hsbc.com.my/wealth/insights/fx-insights/gbp-resilient-but-two-key-risks/