like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

China in Focus: China-US summit: Trade and investment boosts

Key takeaways

- The constructive tone at the first China-US presidential summit of the year was backed by concrete actions.

- Upside surprises from possible tariff cuts on “non-critical” goods and progress on a Board of Investment.

- The summit should boost business confidence, with more engagement scheduled later this year.

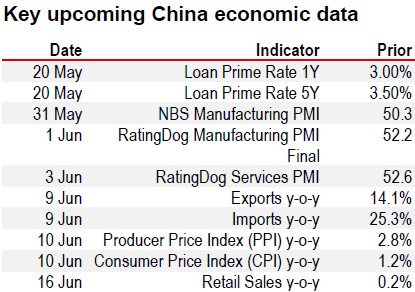

China data review (April 2026)

- Retail sales slowed to 0.2% y-o-y in April, mainly due to a high base from last year and some pullback in the scale of trade-in subsidies. The weakness was concentrated in goods, with auto sales (-15.3% y-o-y) the biggest drag, weighed down by the partial removal of new energy vehicle purchase tax exemptions. By contrast, services consumption remained more resilient, with the services production index up 4.3% y-o-y in April.

- Fixed asset investment fell 9.4% y-o-y in April, marking a clear loss of momentum after a stronger Q1. The slowdown was broad-based, with manufacturing (-4.3%) weighed down by global uncertainties and softer domestic demand, infrastructure (-3.0%) affected by a softening of the pace of government bond issuance, and property (-19.6%) continuing to stay weak.

- Industrial production moderated to 4.1% y-o-y in April (from 5.7% in March) largely reflecting still weak domestic demand and a stronger pass-through from higher oil costs. Instead, external demand and high-tech manufacturing were primary drivers, as seen in the outperformance in auto and electronics production, consistent with the ongoing export strength.

- CPI was broadly stable in April, up 1.2% y-o-y, with the impact of the energy shock mainly concentrated on energy components while food items turned into a drag. PPI surged to 2.8% y-o-y driven by rapid oil price pass-through, AIdemand and anti-involution measures. Early signs of cost pass-through suggest downstream sector responses to core CPI will be key to monitor.

- Exports rose 14.1% y-o-y in April, regaining momentum as seasonal distortions faded, with strength supported by global AI demand, China’s competitiveness in transport-related goods and lower US tariffs. Imports increased 25.3% y-o-y driven by AI-driven demand and industrial upgrading while rising energy and copper prices also pushed up their import values.

China-US summit: Trade and investment boosts

The first China-US presidential summit of the year was to all intents and purposes a success, with President Xi noting that relations had reached “constructive strategic stability” and President Trump stating that the relations would be “better than ever before”. The positive messaging is supported by concrete actions, although some details still need to be hashed out. Agreements and discussions were broad-based, covering areas from trade and investment to market access, fentanyl and geopolitics (Table 1).

Source: White House, Xinhua, CNBC, Bloomberg, Reuters, HSBC

The themes were within our expectations, but there were still some upside surprises. For one, a potential reduction in tariffs in areas deemed “non-critical and non-strategic” could cover c10% of US imports from China (based on 2025 figures). This could help revitalise some direct exports to the US, which have fallen 10% year-to-date y-o-y (albeit a softer pace than last year’s 20% decline).

Secondly, more concrete discussions around the setting up of a Board of Investment exceeded our expectations – we originally thought it would take more exchanges to reach such an understanding. The US administration is open to more Chinese investment in its manufacturing industries provided it does not involve sensitive areas. Ultimately, there will still need to be more details and sufficient guardrails around investments, but we see more potential for re-engagement along this front. Outbound Direct Investment (ODI) flows to the US accounted for 3.5% of total Chinese ODI in 2024, compared with a peak of 8.7% in 2016.

President Trump’s business delegation included CEOs and leadership of some of US’s largest companies, ranging from technology and semiconductor companies to agriculture and finance. The White House readout emphasised discussions on improving market access for US firms, in line with China’s medium and longer-term goals of higher-level opening up, as highlighted in the 15th Five Year Plan. By the end of President Trump’s visit, no major deals had been signed, but we expect agreements to be finalised in the coming days and weeks.

Ultimately, the successful summit should help restore some business confidence, with broad-based discussions and agreements building on the momentum established in Busan six months ago. This sets the stage for more constructive engagement, including potentially at least three more presidential summits this year: an invitation for President Xi to visit the White House on 24 September, the APEC summit in November in Shenzhen, and the G20 summit in December in Miami.

Source: LSEG Eikon

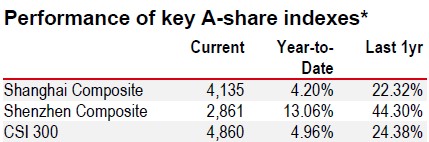

* Past performance is not an indication of future returns

Source: LSEG Eikon. As of 15 May 2026, market close

https://www.hsbc.com.my/wealth/insights/market-outlook/china-in-focus/china-us-summit-trade-and-investment-boosts/