like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: FX puzzles: CAD and JPY

Key takeaways

- The CAD has not capitalised on higher oil prices…

- …probably because of Canada’s non‑US export constraints.

- JPY intervention may work if it comes alongside BoJ tightening and lower oil prices.

FX puzzle 1: Why hasn’t the CAD gained much even with higher oil prices?

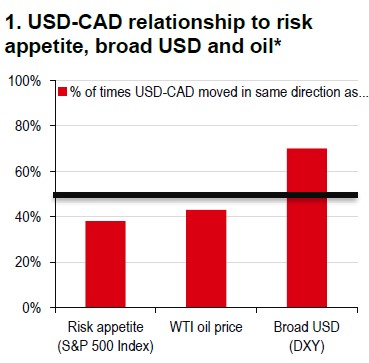

Canada should, in theory, benefit from higher oil via improved terms of trade and energy revenues. In practice, Canada’s ability to monetise global price spikes is constrained by limited liquefied natural gas (LNG) and crude export capacity to Europe and Asia. As a result, a large share of Canadian energy exports remains US‑centric and often trades at a discount, reflecting pipeline bottlenecks and limited west‑coast egress. This structurally caps the CAD’s oil sensitivity: in FX, USD-CAD is typically driven more by broad USD (DXY) moves than by oil prices (Chart 1).

Moreover, the largest oil spikes are often supply-shock events that coincide with risk aversion and USD strength, which can cap CAD upside. In today’s context, even if a prolonged Strait of Hormuz blockade pushes oil prices sharply higher, the CAD may not benefit much.

Source: Bloomberg, HSBC *based on daily changes over last 20 years

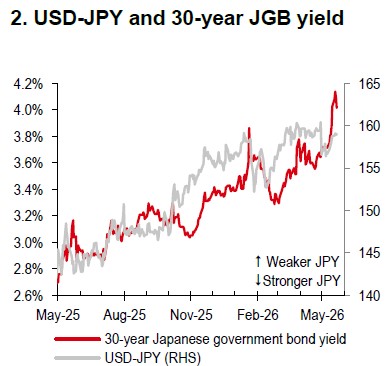

Source: Bloomberg, HSBC

FX puzzle 2: Can intervention keep USD‑JPY below 160?

The key lesson from 2024 is that intervention without policy follow‑through tends to lose impact quickly. In practical terms, intervention alone is unlikely to keep USD‑JPY below 160 for a prolonged period of time. It is more effective when supported by broader conditions − such as a Bank of Japan (BoJ) rate hike and lower oil prices − which together could help USD‑JPY grind lower over time.

However, fiscal concerns may re-emerge and complicate the near-term outlook. These risks could surface in late May, linked to supplementary budget discussions, and/or in June, when Japan releases its annual medium‑term economic and fiscal policy guidelines, expected to be Prime Minister Takaichi’s first. Such developments could push long‑dated Japanese government bond (JGB) yields higher (Chart 2), reinforcing the view that underlying domestic pressures remain persistent. Overall, even with intervention, USD-JPY may struggle to establish a clear downward trend over the near term unless supportive policy and external conditions align.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/fx-puzzles-cad-and-jpy/