like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: USD, EUR, and NZD: Geopolitics and rates

Key takeaways

- The USD is likely to remain range-bound over the near term amid geopolitics.

- The EUR appears to lack a clear directional path.

- The RBNZ’s hawkish hold has buoyed the NZD, while global risk sentiment dominates.

The US and Iran have reached a tentative deal to extend a ceasefire by 60 days, pending President Trump’s signoff; the deal would require Iran to remove all mines from the Strait of Hormuz within 30 days (Bloomberg, 29 May). But, unless there is a clear resolution to the Middle East stalemate, the USD is likely to extend its recent sideways trend and remain range-bound over the near term. The geopolitical impasse is allowing other factors, alongside energy prices, to play a larger role in FX.

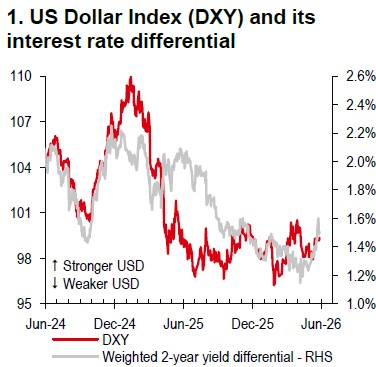

Key theme: Interest rate differentials

Over the coming weeks, interest rate differentials are likely to be the primary market focus. The Federal Reserve (Fed) is still shifting from dovish to more hawkish, whereas this transition is already largely priced in for Europe. This should help underpin the USD (Chart 1) but may not be sufficient on its own to trigger a sustained USD rally.

EUR: Limited scope for a standalone move

With a steady USD as the backdrop, there appears to be limited scope for a sizeable, EUR-specific move. Markets are pricing in around 60bp of the European Central Bank (ECB) hikes by year-end (Bloomberg, 28 May). However, with growing signs of weaker activity (Chart 2), it may be difficult for the ECB to deliver a path that is materially more hawkish than current expectations. The EUR reaction to a less hawkish ECB is uncertain − markets may favour growth support or reprice lower on carry considerations, but the balance of risks is to the downside for now.

Source: Bloomberg, HSBC

Source: Bloomberg, HSBC

NZD: Policy expectations and risk sentiment

The NZD is now in focus after the Reserve Bank of New Zealand (RBNZ) held rates at 2.25% on 27 May in a finely balanced decision, with a hawkish signal via a higher projected rate path (including a 25bp hike in 3Q26, at least one in 4Q26, and a gradual rise towards 3.3% by 4Q28). Our economists expect RBNZ tightening to begin in 3Q26, followed by another hike in 4Q26, and three additional increases, taking the policy rate to 3.50% by 3Q27. Market pricing is more hawkish, with around three hikes fully priced in by end-2026 (Bloomberg, 28 May). Beyond rates, the NZD should remain highly sensitive to global risk sentiment over the near term.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/usd-eur-and-nzd-geopolitics-and-rates/