like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

Macro Monthly: Hard data holding up for now

Key takeaways

- The Middle East conflict is increasingly feeding through to inflation, particularly energy related components…

- …leading to weaker business and consumer survey data, but hard data are still holding up for now.

- We expect rate hikes in the eurozone, UK and Japan while the US is likely to be in wait-and-see mode.

We are now more than 100 days into the US-Iran conflict, and its effects are now showing up in the inflation data. While a framework deal was agreed at the end of May for a 60-day ceasefire, to allow negotiations on Iran’s nuclear programme (BBC, 31 May 2026), air strikes between Iran and Israel continue. It is unclear at the time of writing when a final agreement will be reached. For the global economy, the key uncertainty is how quickly the Strait of Hormuz can reopen, but even if a reopening happens soon, there will still be scars through commodity markets for some time.

Cost pressures

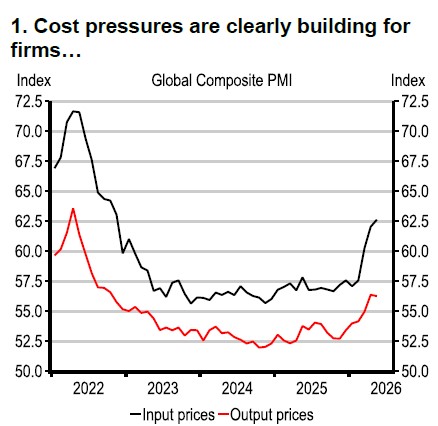

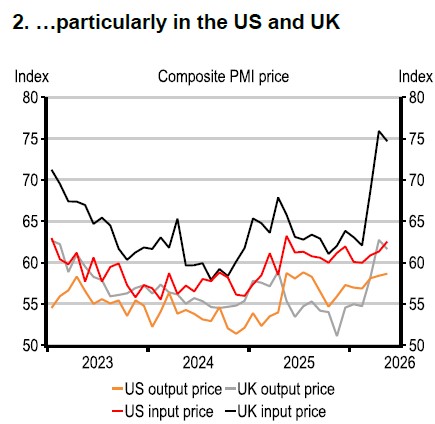

Oil shipments through the Strait of Hormuz remain limited and the IEA has flagged the risk of oil inventories running out soon. That poses substantial upside risks to oil prices. In the CPI data across the world we’ve had for April and May, we can see a clear rise in energy-related components – such as retail petrol prices, air fares, and broader household energy prices – but core (non-transport) inflation has been much more subdued. In addition, the heightened risk of El Niño could add further pressure to food prices and help to keep headline inflation elevated for several more months. We continue to watch for signs of the clear cost pressure for businesses, as evident in the PMI surveys (charts 1 and 2), being passed on in more broad-based inflation.

Source: S&P Global, Latest data: May 2026

Source: S&P Global, Latest data: May 2026

Meanwhile, survey indicators such as PMIs, and other business and consumer sentiment measures, point to weaker confidence, signs of front-loading, and subdued demand conditions.

Robust hard data

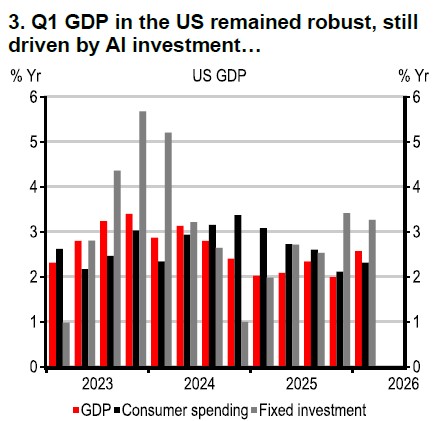

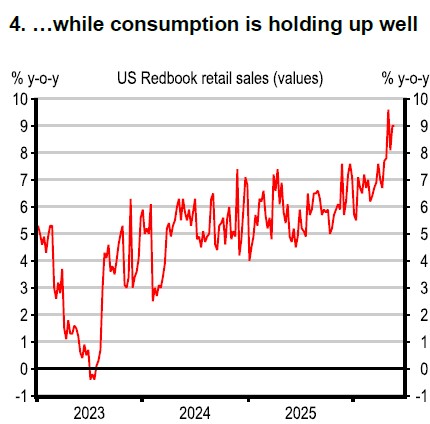

However, hard data have yet to reflect this slowdown in many countries, particularly the US, where consumption and the labour market appear resilient. Q1 GDP data across the world was reasonably strong, buoyed by a combination of consumption, and AI-related investment and exports (particularly in Korea, Taiwan, and the US). This is likely to be the calm before the storm, with the impact of the supply chain and inflation shocks from the Middle East yet to hit much of the activity data, particularly in Southeast Asia. Activity has slowed in mainland China, and weak domestic data are at odds with a rebound in exports. Still, plans to expand public services access to migrant workers should give a boost to consumption in the medium term.

Source: BEA, Latest data: 2026 Q1

Source: Redbook Latest data: May 2026

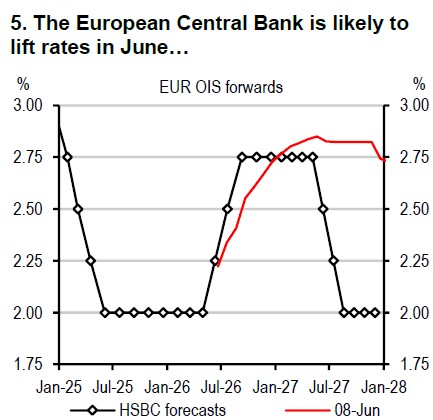

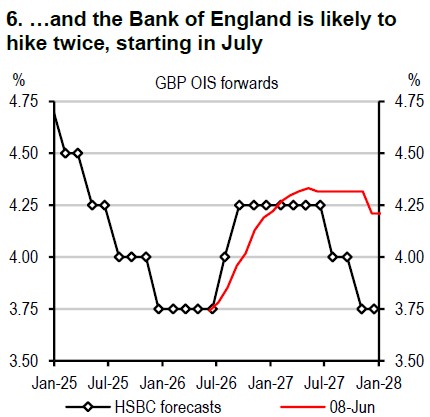

Rate hikes

These dynamics have complicated the policy outlook. Central banks in Australia, Norway, Indonesia, and the Philippines have already raised policy rates. We expect other major central banks, such as the European Central Bank, Bank of England, and Bank of Japan, to follow. By contrast, the US Federal Reserve is likely to remain in wait-and-see mode, with a close eye on the data.

Source: Bloomberg, Latest data: 8 June 2026. Note: OIS = Overnight Index Swap

Source: Bloomberg, Latest data: 8 June 2026. Note: OIS = Overnight Index Swap

Source: Bloomberg, HSBC.

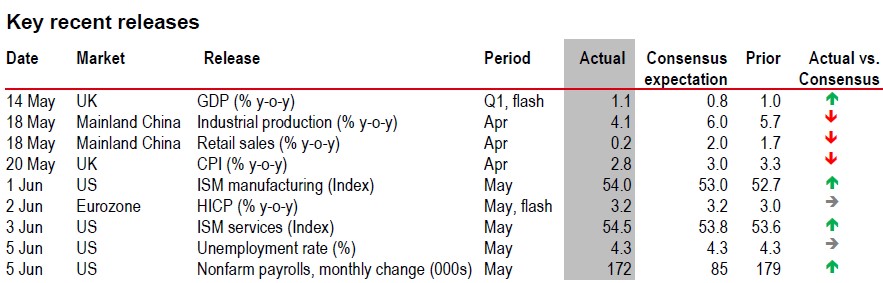

⬆ Positive surprise – actual is higher than consensus, ⬇ Negative surprise – actual is lower than consensus, ➡ Actual is in line with consensus

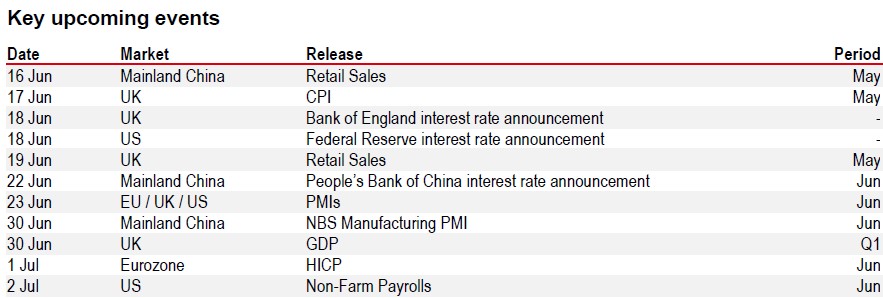

Source: LSEG Eikon, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/macro-monthly/hard-data-holding-up-for-now/