like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

China in Focus: China’s Urbanisation 2.0 – A boost to domestic spending

Key takeaways

- Migrants living in cities are expected to gain access to basic public services, making it easier for them to settle long term.

- A stronger safety net could lift spending by migrant workers and their families, who save c18ppt more than urban peers.

- That could add c0.8ppt to 1.3ppt to annual GDP by 2030 with higher consumption supporting activity and job creation.

China data review (May 2026)

- Retail sales fell for the first time since December 2022, down 0.6% y-o-y in May, as the earlier lift from policy support faded and auto tax exemptions were withdrawn. Auto sales slid 16.1% y-o-y (the largest drag at -1.5ppt) while a high base for consumer goods trade-ins, and ongoing pressure in the property sector and labour market continued to weigh on consumer confidence.

- Industrial production rose 4.5% y-o-y in May, supported by robust exports, AI-related demand and ongoing industrial upgrading, with high-tech industries still leading as the main growth driver. Meanwhile, weaker performance in nonmetallic mineral products and ferrous metals production reflects the slowing momentum in infrastructure and property investment.

- Fixed asset investment was again the key disappointment, falling 12.5% y-o-y in May, the fastest fall since December, as all key components stayed in contraction. Property investment dropped 24.4% y-o-y as the sector remains under pressure despite recent improvements in major cities, while infrastructure investment was down 9.1% y-o-y due to slower direct fiscal support.

- CPI was unchanged at 1.2% y-o-y in May, with energy prices still a key driver while core CPI eased slightly to 1.1% y-o-y as food prices remained a drag (food -1.7% y-o-y, pork -16.1% y-o-y). PPI accelerated to 3.9% y-o-y in May, again driven by higher global oil prices (Brent +62% y-o-y), strong AI-related demand, anti-involution initiatives and non-ferrous metals manufacturing.

- Exports rose 19.4% y-o-y in May, sustaining double-digit growth, while imports were up 27.4% y-o-y, both exceeding market expectations. Strong global AI demand continued to support both flows, but a stabilising China-US trade relationship also boded well for direct exports to the US (+35.4% y-o-y). China’s manufacturing competitiveness continued to underpin exports of capital goods.

China’s Urbanisation 2.0 – A boost to domestic spending

China’s State Council recently outlined a new urbanisation direction designed to help rural migrants not just move to cities for work, but also to settle there long term and increase consumption. The change grants migrants access to basic public services based on their permanent residence, instead of their hukou, China’s household registration permit system.

What’s changed?

Six new priority areas have been set for supporting migrants: ensuring access to education for migrant children; expanding coverage of public rental housing; improving social insurance based on the place of employment; providing medical care based on residence; strengthening employment-related public services; and enhancing basic social safety nets. Collectively, these measures aim to reduce migrants’ precautionary saving and support higher consumption.

Why it matters?

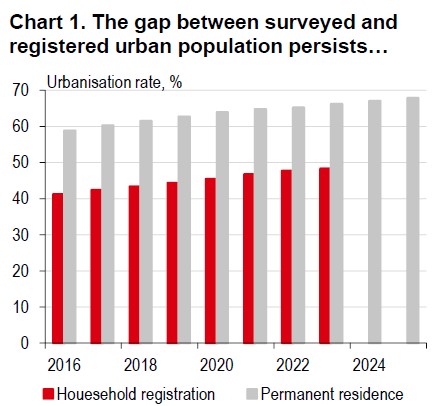

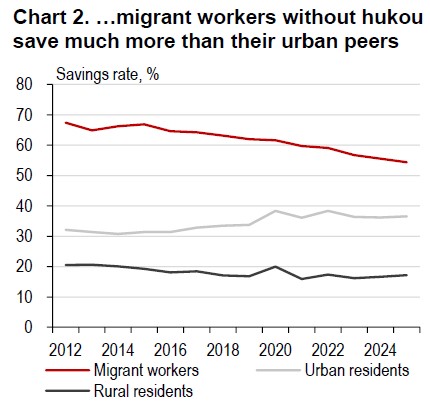

China’s surveyed urbanisation ratio reached 67.9% in 2025 but only half of urban residents – those with hukou status – can access public services such as schools, basic pension schemes and public housing. About 131m migrant workers (c170m including family members) live in cities but save far more than their urban peers (54% vs. 36%) due to limited access to these services. We estimate that extending public service eligibility to permanent residence could unlock consumption, adding roughly 0.8-1.3ppt to annual GDP growth by 2030, while lifting investment needs and potentially creating a virtuous cycle for domestic demand.

Source: Wind, HSBC

Source: Wind, HSBC Estimates

But integrating migrants into cities is expensive. Researchers from China’s Centre for Urban Development estimate the cost of settling one urban resident as cRMB110k (Gov.cn, 28 June 2022). A 1ppt rise (c14m people) implies cRMB1.54trn (1.1% of 2025 GDP) in extra public spending. However, not all costs are upfront: pensions (35–45% of total costs) are back-loaded, while the near-term strain is most visible in public housing and related infrastructure (12–18%).

Which cities will benefit?

Benefits are likely to be concentrated in net-inflow city clusters (where the jobs are), reinforcing the pull of major urban agglomerations. Inland provincial capitals, such as Hefei, Guiyang, Changsha, have seen strong inflows in recent years, reflecting a more attractive balance between job opportunities and affordability. The housing market impact will largely depend on policy support: broader access to public rental housing and provident fund coverage could support demand, but the bigger swing factor is funding. Central government funding and co-ordination will determine whether cities can scale their social housing supply.

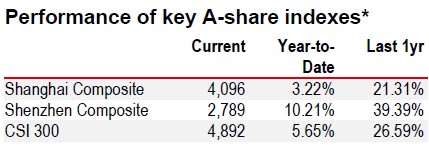

Source: LSEG Eikon

* Past performance is not an indication of future returns

Source: LSEG Eikon. As of 15 June 2026 market close

https://www.hsbc.com.my/wealth/insights/market-outlook/china-in-focus/chinas-urbanisation-a-boost-to-domestic-spending/