like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

FX Viewpoint: USD, EUR, and CAD: Growing risks

Key takeaways

- FX remains driven by geopolitics and central banks’ next steps.

- After the ECB’s stagflation rate increase, the EUR was broadly unchanged, though downside risks are building.

- The BoC faces limited pressure to hike, but trade risks remain.

FX is effectively caught in a spin cycle between geopolitical uncertainties and central banks’ next steps. For EUR-USD, market sentiment often matters more than interest rate differentials. At the moment, risk appetite is closely linked to events in the Middle East, which means sentiment can shift quickly and unexpectedly.

EUR: ECB’s stagflation hike

On 11 June, the European Central Bank (ECB) increased interest rates by 25bp, taking the deposit rate to 2.25%. As markets had already expected this move, the EUR showed little immediate reaction. The ECB’s latest economic projections suggest a more challenging outlook amid “major energy shock”, with slower growth and higher inflation − a situation often described as a stagflation dilemma.

Markets are still expecting two further 25bp hikes by end-2026 (Bloomberg, 11 June). If the ECB signals fewer hikes than expected, the EUR’s support from rates may fade. As such, downside risks for EUR-USD are increasing, and the outlook will depend on both geopolitical developments and US monetary policy outlook.

USD: Fed rates to remain higher for longer?

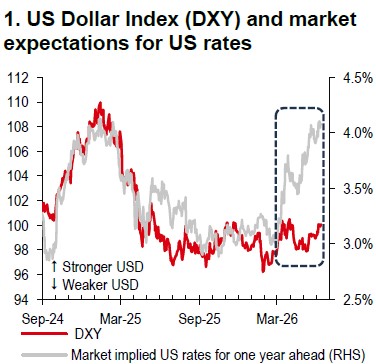

In the US, market expectations have shifted away from interest rate cuts and towards the view that rates may stay higher for longer, with a meaningful possibility of further tightening. Even so, the USD has not strengthened significantly so far (Chart 1). For the USD to gain more support, markets are likely to need a clearer signal from the Federal Reserve (Fed) − particularly through its forward guidance. If the Fed provides a hawkish signal, it could be a key turning point for the USD.

Source: Bloomberg, HSBC

Source: Bloomberg, HSBC

CAD: No urgency for rate hikes, but trade risks remain

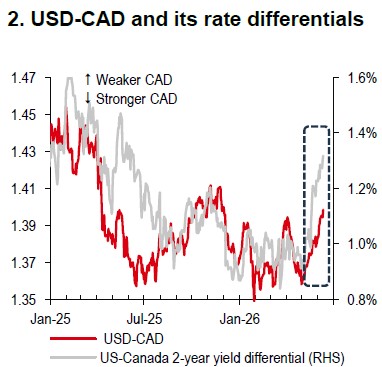

Compared with the ECB, the Bank of Canada (BoC) appears less exposed to a severe stagflation scenario. Recent data point to an improving labour market and limited evidence of broader inflation pressures. Our economists expect the BoC to hold policy steady this year. The CAD is trading somewhat stronger than rate differentials imply (Chart 2), but it remains sensitive to uncertainty around a potential review of the US-Mexico-Canada Agreement (USMCA) after July. Overall, USD-CAD is likely to edge lower in the months ahead.

https://www.hsbc.com.my/wealth/insights/fx-insights/fx-viewpoint/usd-eur-and-cad-growing-risks/