like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Economic Updates

ASEAN in Focus: Pushing ahead

Key takeaways

- ASEAN’s economies are facing multiple shocks, from a brewing El Niño to US tariff uncertainty…

- …yet activity is set to prove surprisingly resilient, supported in parts of the region by surging demand for AI hardware.

- Rising price pressures are posing a risk, as do growing budget deficits, but growth should continue to trot along.

Indonesia’s economic performance remains stronger that market sentiment suggests, with a policy pivot underway to strengthen confidence. Thailand has seen investment bounce of late, but the lift in growth may not prove durable. Malaysia is riding the AI wave, but a possible election could sap reform efforts. The Philippines suffers from a surge in prices and fiscal inaction, even if its fundamentals remain solid. Vietnam harbours ambitions for more, even if growth is already at an impressive pace given energy and tariff headwinds. Singapore remains its resilient self, chugging along with relative ease, and taking a growing share of the AI boom.

Economy profiles

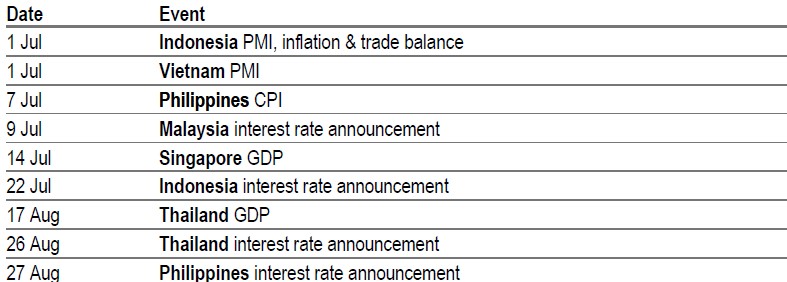

Key upcoming events

Source: LSEG Eikon, HSBC

Indonesia

Market strain, policy pivot

There is much attention on Indonesia lately. Across the major asset classes - equities, bonds and FX - Indonesia has underperformed the broad Emerging Markets (EM) index YTD. A cursory glance suggests that even though markets have not performed too well, the economy is chugging along fine. GDP rose 5.6% in the quarter ending March, higher than the 5.1% growth in 2025. And even though inflation has risen, it remains well within the 2.5-3.5% range.

A deeper review, however, suggests that the economy has started to gradually reflect the impact of the energy shock, and markets may be partly reflecting that. On growth, the latest readings show a fall in retail spending, consumer sentiment and export orders. There has been a significant amount of frontloading in fiscal expenditure, and belts may need to tighten in subsequent months to meet the 3% fiscal cap. We forecast GDP to grow 4.7% y-o-y in 2026 (versus 5.1% in 2025).

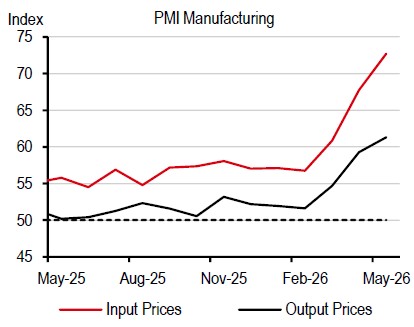

PMI input prices have risen quickly and are gradually pushing up output prices. We forecast inflation to average 3.5% in 2026 (versus 1.9% in 2025). The latest trade data shows a fall in the monthly surplus, with export volumes falling even as import volumes shot up. Meanwhile capital inflows remain sluggish, weighing on the exchange rate.

Supply shocks such as rising energy costs and adverse weather are always tricky to deal with because they come with trade-off. Generally, inflation rises and growth falls during these shocks. Often, policymakers have to choose between the two.

Some observers may see the Indonesian rupiah (IDR) as the primary challenge to address. The underlying driver of the IDR’s depreciation seems to be the balance of payments, which is likely to post its second negative annual reading in 2026. It’s tempting to argue that Indonesia does not face a current account problem, given the modest shortfall of -0.1% of GDP in 2025, and that the bigger concern is weak capital inflows, which came in at -0.3% of GDP in 2025. But, in practice, these two factors are interlinked. A low current account deficit can reflect subdued investment demand. Indeed, we find that corporates are cash rich but reluctant to invest. And weak investment and growth prospects can hurt capital inflows.

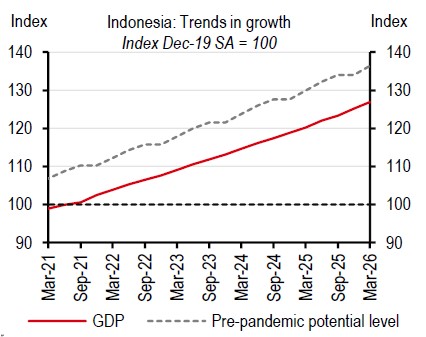

Indonesia’s persistent negative output gap

Source: CEIC, HSBC

Price pressures are rising

Source: CEIC, HSBC

Malaysia

Resilience is a virtue

Until the Middle East conflict, the Malaysian economy was in a “Goldilocks” stage, with strong growth and stable inflation. But the conflict increases the possibility of downside risks to growth and upside risks to inflation, even if Malaysia has demonstrated more resilience than regional peers, as it is not only a net energy exporter, but also a key beneficiary of the sustained AI cycle. This is not to say that Malaysia will be insulated from the energy shock, but the impact should be smaller than for other economies, which are heavily dependent on energy imports from the Gulf.

Malaysia has made a strong start to the year, with GDP up 5.4% y-o-y in 1Q26. While construction cooled from double-digit to single-digit growth, the sustained strength in manufacturing and services has more than offset the moderation. Exports remain strong, thanks to the ongoing AI-driven tech cycle. On a 3-month moving average basis, Malaysia’s electronics exports surged to 30% y-o-y.

Elsewhere, inflation has been well-behaved for a sustained period of time, averaging only 1.7% y-o-y in the first four months of 2026. This gives Malaysia one of the lowest inflation prints in ASEAN, significantly lower than peers like the Philippines and Vietnam.

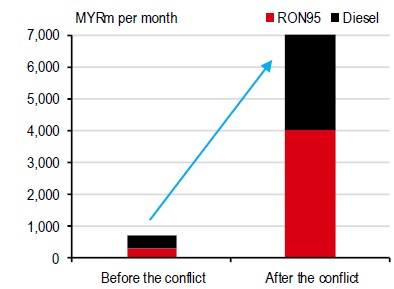

In the face of elevated energy prices, it is not hard to understand why: Malaysia is blessed with the region’s lowest petrol prices. Using the most common RON95 price as a gauge, Malaysia’s RON95 remains at MYR1.99/l (USD0.5/l), 1/10 of that in Hong Kong, 1/5 of Singapore, 1/3 of Thailand and 1/2 of Vietnam. However, this is primarily due to heavy subsidies: RON95 at the market rate, or the unsubsidised rate, is twice that of the subsidised price.

This comes with significant fiscal costs. The monthly subsidy bill for energy has risen tenfold from MYR700m to MYR7bn due to the conflict. The hefty subsidies raise questions on what comes next for the RON95 policy, as it imposes huge pressures on Malaysia’s fiscal coffers. But the timing of any potential adjustments is also tricky, as the general election is approaching fast.

Overall, we maintain our GDP growth forecasts at 4.5% for 2026 and 4.7% for 2027. Bank Negara Malaysia (BNM) is one of the few Asian central banks to raise its 2026 growth forecast range, increasing it from 4-4.5% to 4-5%. On inflation, we recently revised upwards our inflation forecast to 2.5% (from 2.1%) for 2026, and to 2.7% (from 2.3%) for 2027. However, we do not believe the price pressures are significant enough to prompt BNM to hike. We keep our long-held view that BNM will likely stay on hold in our forecast horizon throughout 2027.

Malaysia has been benefitting handsomely from the sustained AI-driven tech cycle

Source: CEIC, HSBC

Its petrol subsidy skyrocketed ten-fold to MYR7bn per month after the conflict

Source: Malaysia MoF, HSBC

Philippines

Hanging in there

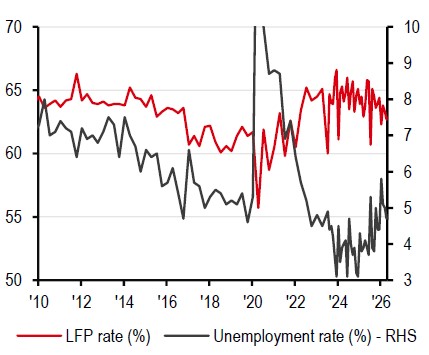

Stagflation appears to be emerging in the Philippines. For one, growth continues to sour. In 1Q26, growth came in at 2.8% y-o-y, stumbling to its slowest pace since 2009, excluding the COVID-19 pandemic. The culprits of the slowdown remain the same: public capital disbursements continue to fall at a significant rate while the uncertainty around public spending has led to households and businesses pulling back on their expenditures. Savings are up, and investment is down.

Understandably so – households can weather tough times by putting aside a larger portion of their incomes during good times. That good time was 2025, when wages grew 7% on average while inflation was only 1.7%. However, instead of enjoying the increase in purchasing power by spending more, households chose to save. The share of households reporting that they were able to save before the energy shock in March 2026 was even higher than pre-pandemic levels, with the more vulnerable, low-income households leading the increase.

Unfortunately, this slowdown in demand has already spilled over to the labour market. The unemployment rate in the Philippines has risen above 5%. And soon, households and small businesses may need to dip into the savings they have recently accumulated.

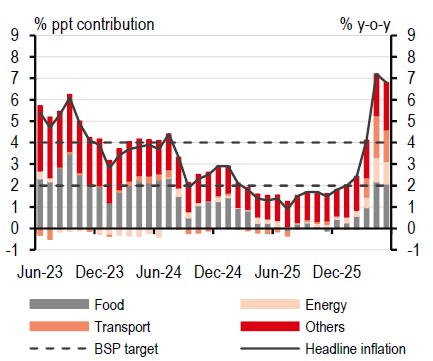

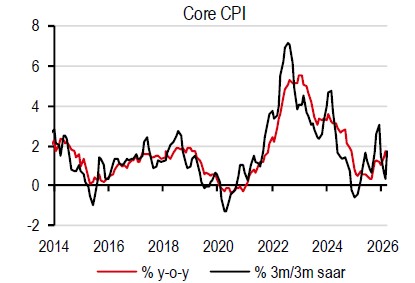

This is because prices continue to rise amid slow growth. Currently at 6.8% y-o-y, headline inflation in the Philippines is the highest in the ASEAN region. The surge in energy prices has already spilled over into core CPI, with core inflation accelerating above the central bank’s 2-4% target band. However, the outlook is set to become tougher, with price pressures on food − due to higher fertilizer prices and El Niño − expected to intensify in the coming months. We expect growth to come in well below potential in 2026 and 2027, at 3.4% and 4.8%, respectively.

But the Philippines is hanging in there. Once the energy shock normalises, financial markets in the Philippines are likely to recover quickly. This is because the fiscal response has remained prudent, as officials opted for targeted welfare measures. In addition, a healthy degree of “demand destruction” should eventually come to the fore. Without controls, energy prices in the Philippines have reflected the true scarcity of commodities. Growth may be below potential, but once the dust settles, public debt and the current account is likely to remain manageable and resilient.

With construction demand falling, the labour market has tightened…

Source: CEIC, HSBC

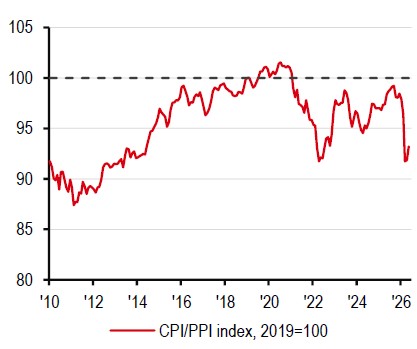

…all while inflation in the Philippines is rising across all major categories

Source: Macrobond, HSBC

Singapore

Treading with prudence

Singapore, a developed market (DM) growing like an emerging market (EM), has demonstrated impressive resilience amid the Middle East conflict. In 1Q26, GDP growth of 6% has placed it as the second-fastest growing economy in ASEAN, just after Vietnam. But beyond the strong y-o-y print, Singapore’s growth momentum was equally strong, reflecting the benefits of a diversified economy.

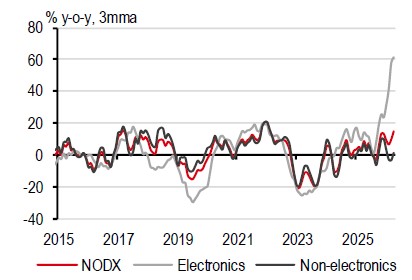

Alas, manufacturing momentum declined in 1Q, but it was more of a healthy pull-down from previous sustained manufacturing strength, supported by the AI-driven tech upcycle. In fact, based on high frequency indicators, the electronics trade remains exceptionally strong. On a three-month moving average basis in April, electronics non-oil domestic exports (NODX) accelerated to over 60% y-o-y, pushing headline NODX close to 15% y-o-y.

But it’s not only about AI. Singapore’s resilience comes from its broad-based growth. For one, the construction sector saw growth of over 11% y-o-y in 1Q, reflecting Singapore’s push for large-scale public infrastructure. Meanwhile, the services sector also accelerated on a y-o-y basis, benefitting from robust wholesale and retail trade as well as the finance sector.

There is no time for complacency, as downside risks to growth linger, induced by the energy shock. Singapore is in a much better fiscal position than EM peers to provide much-needed relief but it takes a cautious and measured attitude. Overall, given the upside surprise in 1Q26 and the sustained AI cycle, we recently upgraded our growth forecast to 3.3% (from 2.9%) for 2026, putting it at the upper end of the government’s growth forecast range of 2-4%. We forecast 2027 growth of 2.5%.

Outside of growth, inflation has been well-behaved, despite the energy shock. Core inflation, the Monetary Authority of Singapore (MAS) preferred inflation gauge, grew only 1.4% y-o-y on average in the first four months of 2026. But the impact from higher oil prices is likely to be more evident from 3Q26, as there is usually a quarter lag from global energy prices to core inflation. Thus, the inflation impact will be more evident in 2H26.

We also upgraded our core inflation forecast to 2.0% (from 1.8%) but revised down our headline inflation forecast to 2.2% (from 2.4%) for 2026. No doubt, inflation has re-emerged as a priority for the MAS. Given the current inflation trajectory, the MAS is more likely to take its time to assess the inflation impact, rather than resorting to a back-to-back tightening move in July.

Singapore’s electronics non-oil domestic exports (NODX) have seen a jump in growth

Source: CEIC, HSBC

Singapore’s core inflation momentum has been volatile, but upside risks linger

Source: CEIC, HSBC

Thailand

Policy clockwork

Thailand’s economy had some degree of momentum before fuel prices spiked on 23 March 2026, the day the government lifted its price ceilings on fuel. Growth in 1Q26 exceeded expectations, accelerating to 2.8% y-o-y despite the turmoil in the Middle East. Sectors and industries that are part of the data centre and AI supply chains were particularly buoyant. Goods exports from Thailand surged 15.5% y-o-y − the fastest since exports boomed during the COVID-19 lockdowns – with most of the outperformance seen in electronics. Thailand is a major producer of printed circuit boards and hard disk drives, two of the many types of hardware that make up the sophistication of a data centre.

Private investment, too, grew by double digits as some of the digital investments committed over the past two years (most being AI-related) finally materialised. Business confidence, especially among large firms, was upbeat as Thailand garnered a renewed sense of political stability after the February 2026 general election. Private consumption also remained punchy with consumers frontloading their automobile purchases ahead of the expiry of the EV 3.0 subsidy scheme.

We expect the economy to ride this momentum through fiscal policy. The government has issued a THB400bn loan decree (2.1% of GDP), half of which will be used to finance consumer subsidies. The other half will be used to finance Thailand’s energy transition. Given the size of the stimulus, we have recently revised our 2026 growth forecast to 2.2% (from 1.6%).

Will the Thai economy defy the challenges brought by the Middle East conflict?

There are cracks that need to be monitored. For one, manufacturers that do not benefit from the ongoing AI boom still face intense competition from Chinese imports. Private consumption should also slow once the consumer subsidies are wound up, while households continue to face liquidity constraints. As a result, businesses have found it difficult to raise the prices of the goods and services they sell despite the jump in input costs. With profit margins squeezed, there is likely to be less incentive to invest later in the year and into the next.

Overall, the growth outlook has improved in 2026, but 2027 is likely to remain tough. We recently revised our 2027 growth forecast downwards to 1.7% (from 2.6%). And, given the difficulty in passing higher costs on to consumers, we expect inflation to ease back to below 2% y-o-y as early as 2Q27.

Firms have found it difficult to pass the higher cost of inputs on to consumers

Source: Macrobond, HSBC

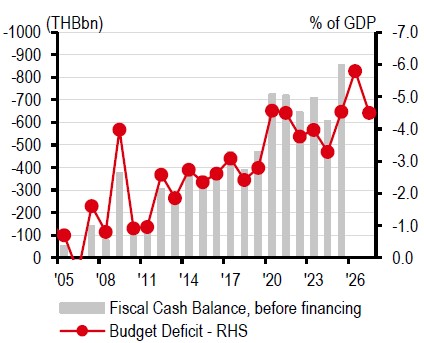

We expect fiscal policy to tighten in 2027 after a decade of widening deficits

Note: *2026-27 are HSBC forecasts. Source: CEIC, HSBC

Vietnam

No room for complacency

Vietnam entered 2026 on a resilient footing. Despite moderating from last year’s 8%, the country saw rather decent growth of 7.8% y-o-y in 1Q26. This easily made Vietnam sustain its position as one of Asia’s fast-growing economies. However, there is no time for complacency, as the Middle East conflict has pushed up energy prices to elevated levels.

Nevertheless, a detailed look at trade data shows Vietnam’s trade resilience. Exports jumped almost 20% y-o-y YTD on average, thanks to booming electronics shipments. While Vietnam’s exposure to chips is rather limited, it has captured more market share in consumer electronics; not to mention that it has the ambition to climb up the value chain, seeing vast potential from its young, knowledge-hungry and tech-savvy workforce.

Despite booming exports, Vietnam’s imports grew even more, rising 30% y-o-y YTD. This is also understandable, to an extent, as Vietnam’s manufacturing sector is rather import-intensive. However, this raises a question about its trade balance. Since December 2025, Vietnam has consistently run a trade deficit, which widened to a record level of USD5.2bn in May. We do not think Vietnam will enter a “twin deficit” situation, as the tourism receipts and secondary income will help. However, we have revised down our current account surplus forecast to 2.2% of GDP, from 6% earlier, for 2026. This could pose depreciation pressure on the Vietnamese dong, which has been holding up surprisingly well compared to others since the start of 2026.

Overall, we forecast GDP growth of 6.5% for both 2026 and 2027. But downside risks are picking up, and depend on how the Middle East conflict evolves. The immediate concern for Vietnam is how to grapple with elevated oil prices. History reminds us of the acute impact of high oil prices in 2022: high oil prices pushed up Vietnam’s inflation, breaching its 4% ceiling for a little less than six months.

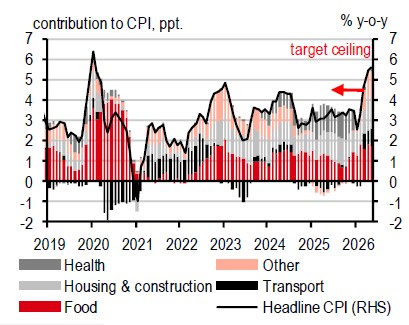

Fast forward to today, Vietnam’s inflation rose sharply to 5.6% in May, breaching the State Bank of Vietnam (SBV)’s 4.5% inflation ceiling for the third month running. While the significant jump in petrol prices was the main culprit, it is important not to ignore the recent hike in food prices. Although Vietnam is a rice exporter, its domestic rice prices are typically influenced by international prices. Overall, we recently revised up our inflation forecast to 5.2% (from 4.6%) for 2026.

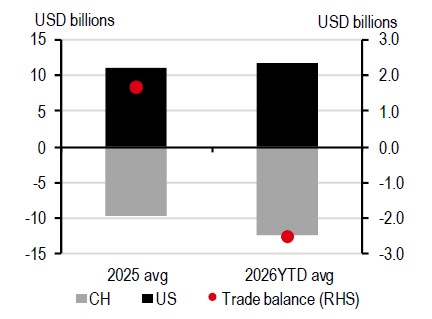

Vietnam has consistently seen a trade deficit since the start of 2026

Source: CEIC, HSBC

Vietnam’s inflation has breached the central bank’s 4.5% target since March

Source: CEIC, HSBC

https://www.hsbc.com.my/wealth/insights/market-outlook/asean-in-focus/pushing-ahead/